Tough environment for stock selection – what’s working for us?

The past 12 months has been an extreme environment for markets in many ways. The disparity in factor performance has been notable globally; growth stocks appear to be as expensive as they have ever been, and value stocks arguably as cheap as they have ever been. Let’s take a look at the equity positions and performance in the Russell Investments Managed Portfolios.

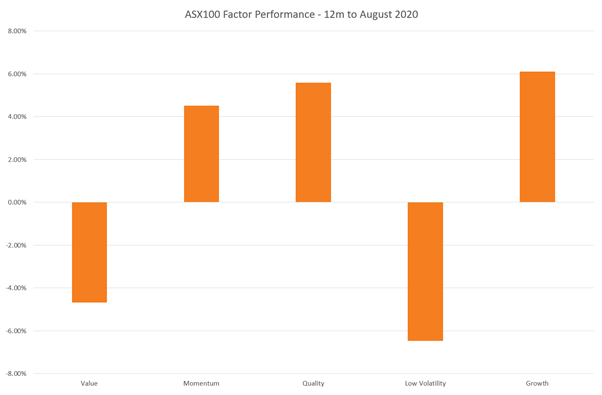

Australian shares invested directly by Russell Investments

The Australian shares component within the Managed Portfolios uses a strategic multi-factor approach to portfolio construction. Over the long term, we believe that there are positive excess return tailwinds associated with stocks exhibiting specific characteristics or factor exposures. The Australian shares component is exposed to momentum, value, low volatility, quality, and growth stocks

It is constructed in such a way that reflects our relative conviction in factor premia in the Australian market over time.

In Australia, the relative valuation between styles has not hindered the continued outperformance of growth and momentum over the past year. For the 12 months to the end of August, growth and momentum stocks had outperformed value stocks by approximately 10%.

Source: Russell Investments, ASX100 universe

Over the past year, the Australian shares component of the Managed Portfolios has outperformed its benchmark (ASX100) by over 100 bps1. Exposure to the materials sector contributed positively as Fortescue Metals, a value and momentum stock, returned over 150% for the period. Goodman Group, a quality and momentum exposure within the Property Trust sector also contributed to excess returns. Quality growth stock Magellan added value over the period, as did growth and momentum stock Xero. Exposure to energy stocks was the main detractor over the period. The managed portfolios stock contributors to excess return were across all factors, which is pleasing in an environment of divergent returns at the aggregate factor level.

Global shares invested through ETFs

The key positions in global shares are overweight positions to emerging market shares (relative to US shares) and shares with smaller market capitalisation. This is mostly achieved through ETF selection.

Last month, the US share market (i.e. S&P 500 index) made new all-time highs surpassing levels last seen in February 2020. The strong rally was led by stocks like Apple, Microsoft and Amazon. We firmly believe that the regional outperformance is unsustainable due to the long-term headwinds of expensive valuations, very high profit margins and lofty sales growth expectations. Conversely, a weaker USD environment and early-cycle recovery point to emerging market equity outperformance.

It will take time for a larger turnaround as accommodative monetary and fiscal policies have provided retail and passive investors with cheap funding to chase these large US stocks. However, we only need to look at the quick selloff in US tech shares in early-September 2020 to see the potential reward for sticking with the underweight position. Our active global sector funds within the dynamic core of the Managed Portfolios (Russell Investments Multi-Asset Growth Strategy Fund) have also benefited recently. This will continue to be one of the key drivers of performance for the multi-asset managed portfolios in the long-term.

Conclusion

Over the last year, the direct Australian shares component has contributed to gains within the Managed Portfolios in a tough environment for stock selection. The global shares allocation within the Managed Portfolios has a large tilt against US shares and we are seeing signs that the unsustainable pace of outperformance is slowing down. Over the long-term, we prefer emerging market shares due to more attractive valuations and long-term growth potential.

1 FactSet. Performance for 12month period to 9 September 2020 is +127 bps vs the ASX100.