UK Election: A Wobbly Win for the Conservatives

- Theresa May’s disappointing victory makes Brexit negotiations more likely to fail

- Equity weakness is likely with a rebound into gilts

- Investors should prepare for increased market volatility as we expect a bumpy road to Brexit

- Russell Investments’ Multi-Asset funds have no structural overweight allocation to UK assets

The campaign

The election campaign turned out to be a lot more interesting than many expected when Prime Minister May announced her wish to hold a snap election. At the time, the Conservatives were almost 20% ahead in the polls and it seemed as though the British public overwhelmingly favoured Theresa May over Labour-leader Jeremy Corbyn to deliver Brexit negotiations. As a result, the media and political analysts widely expected a resounding victory and an increased Conservative majority in the House of Commons to more than 100 seats.

But then the campaigns got under way…To everyone’s surprise the Conservatives were quickly put on the defensive about hot topics like social care, while Labour found traction on issues such as education and housing. This reversal and subsequent narrowing of the polls turned a coronation into a battle.

In the end, however, that battle was still won by the Conservatives.

Brexit negotiations

A disappointing Conservative majority in the House of Commons provides May with limited maneuvering room to negotiate an exit agreement from the European Union and a transition period after Brexit. If a transition period one-to-three years can be agreed upon, it could reduce the risk of the UK crashing out of the EU and help sort out the enormous legal tangle.

What are the implications for UK assets?

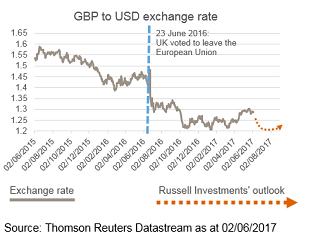

Sterling

Since the referendum on 23 June 2016, the British pound exchange rate has been the best barometer for the market’s perception of the risks and opportunities.

After falling more than 15% in trade-weighted terms during 2016, sterling recovered almost 8% over 2017. However, it quickly fell back by 3% in May as the Conservative polls started to narrow during the run up to the election.

Looking ahead, we think the pound will fall but could recover relatively quickly given the prospect for a softer Brexit (see chart).

Equities

Equity markets will be slightly disappointed initially, but should not be affected in a major way in the medium term. Overall, the outlook for UK stocks is closely linked to global economic prospects.

Gilts

In such an environment, we project that 10-year gilt yields will rise eventually due to the Labour party’s expansionary fiscal policy, which may also cause the rating agencies to review the UK’s credit rating.

Economic outlook

Our bottom line is that whilst this general election result feels like a crucial event for those in the UK, it does not carry with it the same market significance as others have over the past year, namely the French or Italian elections. Indeed, the post-Brexit economy has done well so far, but we continue to believe that the slowdown in corporate and housing investment, in combination with downward pressure on real wage growth, will slow economic growth in 2017 and 2018.