How the Russia-Ukraine war highlights the importance of ESG considerations in FX markets

Could a heightened focus on ESG (environmental, social and governance) factors have prevented investors from experiencing steep losses in Russia-related investments the past few months?

It’s a good question, with some surprising answers.

Following Russia’s unprovoked Feb. 24 assault on Ukraine, sweeping sanctions placed on Russia’s currency and Russian companies have rippled through all asset classes, affecting portfolios across the globe—including those with an allocation to foreign exchange (FX) markets. In some cases, these impacts have been fairly detrimental, with investors’ hard-earned alpha seemingly evaporating overnight.

But what if ESG factors had been taken more into consideration in the weeks leading up to the invasion? What if the governance risks of an exposure to Russian securities had been fully integrated into a currency strategy? Or if increased attention had been paid to the implications that an attack could have on environmental factors, such as an allocation to oil and gas? Would investors have earned higher returns?

We’ll take a look at all of this in short order—particularly as it relates to foreign exchange markets. But first, let’s back up a step and review the basics of what makes a strategy an ESG strategy. Call it ESG 101.

ESG strategies: A review

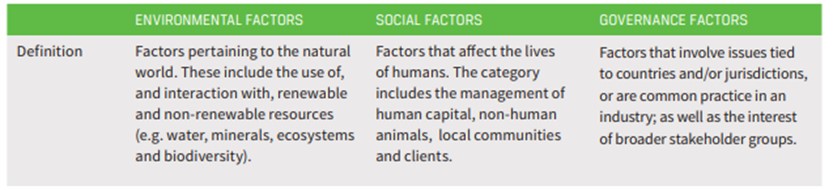

ESG strategies aim to incorporate environmental, social and governance factors within the investment-making decision process. These factors are defined in the table below.

Table 1: ESG factors, defined

Source: CFA Institute

There are a variety of approaches to screening the universe of assets and incorporating ESG factors into such strategies. Let’s take a look at the ESG factors in the context of the ongoing war in Ukraine to help understand the value of such an approach.

The penalties of underexposure to oil and gas: Assessing the environmental factor

Russia is an important provider of energy, being the largest natural gas-exporting country in the world, with a significant supply chain dependency.1 Most ESG strategies typically move capital allocation toward green energy and away from oil and gas, but in a world that’s still heavily reliant on the latter, such an approach can prove costly. Russia’s invasion of Ukraine demonstrates this all too well. Western sanctions imposed in response to the assault on Ukraine have pushed oil stocks up due to supply worries.2 As Russia’s revenue on exports of crude oil rises3, ESG investors with underweights in oil stocks are seeing their portfolio alpha penalized.

Is this something that could have been prevented with a more complete ESG analysis? We would argue so, because when it comes to ESG investing, there’s almost always more than meets the eye. Factoring in ESG considerations into an investment process is often complicated, complex, and—in this case—contradictory. And, as this example shows, when large amounts of money are at stake, the cost of not conducting a comprehensive ESG analysis can be high.

The cost of underweighting defense stocks: Assessing the social factor

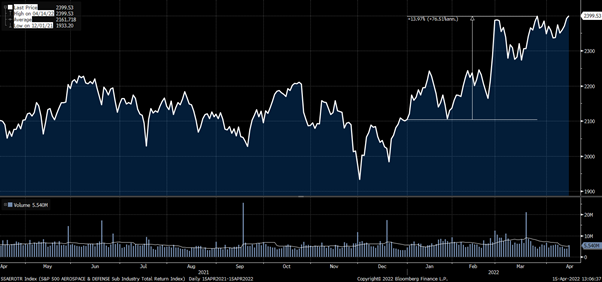

The war in Ukraine has also led to a surge in defense stocks, with the S&P500 aerospace and defense industry rallying over 13% during the first quarter of 2022. Not unlike its oil and gas counterpart, defense is a sector that most ESG strategies typically omit exposure to, as companies in this industry make lethal weapons. After the invasion of Ukraine sparked a need for increased security across the globe, however, investors started reviewing their positions.4

For return-seeking investors, this is another example of the perils of only conducting a surface-level assessment of ESG risks and opportunities. Once again, the Russia-Ukraine war demonstrates there’s more than meets the eye for ESG investors—and that context matters.

Figure 1. S&P500 Aerospace & Defense Total return in USD from 04/15/2021 to 04/15/2022. Graph from Bloomberg.

The risks to currency strategies: Assessing the governance factor

According to World Economics, Russia’s governance data scores a low 21 out of 100.5 Furthermore, MSCI downgraded Russia’s ESG government rating to its lowest rating (CCC) on March 8, forcing some managers to stop new investments in Russia or liquidate existing ones. But low governance scores are nothing new to Russia, which received very low rankings in 2021 on metrics such as global freedom, internet freedom, national democratic governance, civil society and independent media from Freedom House, a U.S.-based non-profit research institute.

The current crisis forces ESG strategies to re-think screening factors. MSCI recognizes that “historic quantitative data used in our methodology are no longer accurate indicators for the level of risk faced by Russia on these key ESG issues”. Typically, ESG factors are based on an analysis of company-related securities, such as equities or corporate bonds. The logic behind this is the ability to influence decision-making of companies by shareholders or stakeholders. Other asset classes, such as currencies, are more complicated to categorize, as they lack the corporate management structures that ESG factors are normally applied to. While currencies are recognized as a separate asset class with the potential for diversification and alpha generation, there is no conventional approach to apply ESG factors on currency strategies.

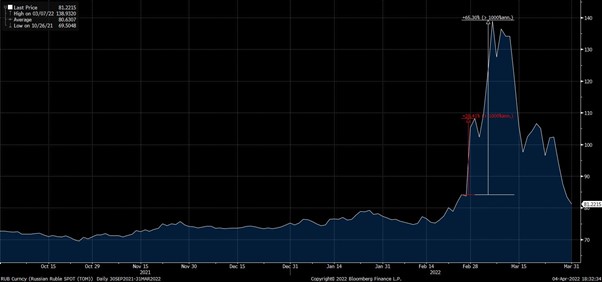

The ruble (RUB) depreciated about 30% against the U.S. dollar after Western nations restricted the free movement of Russia’s currency, as the chart below shows. In addition, most asset managers suspended purchases of Russian securities and reduced their exposures. Currency managers also had to significantly reduce their RUB exposure.

Figure 2. Russian Ruble spot price against USD from 09/30/2021 to 03/31/2022. Graph from Bloomberg.

Could an ESG analysis have made investors more wary of the Russian ruble?

Given Russia’s low governance score, we believe it is likely. Currencies, like other asset classes, can benefit from ESG analysis. ESG factors can be integrated to a return-seeking currency strategy by, for instance, tilting to currencies of countries with higher ESG performance.

What factors might comprise a country’s ESG performance? Environmental factors could include the energy intensity of GDP (gross domestic product) or the currency’s sensitivity to commodity prices. Social factors, meanwhile, could be linked to a country’s education spending and risk of social unrest. Last but not least, governance factors could be linked to political and economic institutions.

The bottom line

In the context of war, ESG investors are facing new challenges and dilemmas, which to some may feel like a step back. The invasion of Ukraine and its impact on ESG factors show that the journey toward a greener, more peaceful environment will be a bumpy, complicated one. We still believe asset managers have an opportunity to explore and incorporate new factors, as ESG investing continues to see an increased demand. At the same time, we strongly recommend working with a strategic partner who understands the complexity of ESG, within a total-portfolio context.

Ultimately, we expect ESG strategies across all asset classes to flourish, and we believe that in foreign exchange markets, ESG factors will only become more important for risk reduction and return enhancement. The implications of Russia’s invasion of Ukraine on investor portfolios demonstrates all too clearly what can happen when ESG is overlooked.

1 As of 2020. Source: Enerdata. https://yearbook.enerdata.net/natural-gas/balance-trade-world-data.html

2 The MSCI Oil, Gas and Consumable Fuels Index outperformed the broad MSCI World index by 5.2% since February 23, 2022 (the day before the invasion). Source: Refinitiv Datastream, as of 6 April 2022.

3Factbox: Russia's oil and Gas Revenue Windfall. Reuters. Retrieved April 4, 2022, from https://www.reuters.com/markets/europe/russias-oil-gas-revenue-windfall-2022-01-21/

4 Hollinger, P. (2022, March 9). Ukraine war prompts investor rethink of ESG and the Defence Sector. Financial Times. Retrieved April 15, 2022, from https://www.ft.com/content/c4dafe6a-2c95-4352-ab88-c4e3cdb60bba

5 Russia's governance factors. World Economics. (n.d.). Retrieved April 4, 2022, from http://dev.worldeconomics.com/ESG/Governance/Russia.aspx