Russia invades Ukraine. What does this mean for investors?

What many feared may happen came true overnight with Russia invading Ukraine from all sides - Crimea, Belarus and Russia.

Events have moved quickly since our update on February 22. It’s unclear whether this is the shock and awe phase of a limited incursion or the beginning of a full-scale invasion that seeks regime change in Kyiv. The invasion represents a humanitarian tragedy with terrible consequences for millions of people. Investment markets are now reacting to the uncertainty created by events. The implications for European and global political stability are a key issue. We are evaluating the portfolio implications of events through our cycle, value, and sentiment (CVS) framework. We’re assessing the risks to our global cycle view from a full-scale invasion. We also continue to monitor our composite sentiment index to judge whether investor psychology has reached an unsustainable level of panic that justifies a more risk-on stance.

At this stage we are closely monitoring the situation and any responses from Western governments, particularly on sanctions. We are waiting to see how the situation unfolds and while there are no immediate plans to alter strategy weightings within the funds, we are monitoring events closely to determine whether any action needs to be taken.

Our Emerging Markets funds had been holding up well until this devastating development. RIC PLC EMEF has maintained its exposure to Russian equities at 3.2% (benchmark weight 2.8%) as of 23 Feb 2022. As mentioned before, most of this exposure is held in depository receipts which is seeing severe selling pressure today. While our allocation to Russia will have a detrimental impact on absolute returns today, the impact on relative returns is somewhat mitigated by the fact we have a lower overweight now to the market than last year. Given the severe decline in markets today and record low valuation levels of our holdings in Russia, most of our underlying managers are not adjusting their Russia exposures, but rather will wait to see the extent of new sanctions and Russia’s response to this.

The fund exposure data shows that there is minimal direct exposure in our global equity funds. The main impact is the “risk-off” sentiment across global capital markets with an obvious “flight-to-quality” taking place (bond yields falling, defensive sectors winning). Energy has also spiked. Market-moving macro events come along every couple of years and our typical approach is to wait for the dust to settle somewhat, avoiding the noise and volatility created by short-term flows, especially when events cannot be predicted. We will remain disciplined in our process and use opportunities seen through our “CVS” lens to re-deploy capital as necessary. A good example would be moving assets from defensives back into cyclicals if the outlook were to improve.

In our fixed income portfolios, our long strategic and actual duration overweights are helping to provide protection as part of our diversified positioning. We are currently holding credit risk levels, which have been underweight to strategic overweight levels, with consideration for tactical adding at attractive valuations.

Within our multi-asset funds our defensive diversifiers (Government debt, USD and JPY exposure, Gold) are delivering on expectations in a risk-off environment and offsetting some of the negative performance coming from our equity book. Due to recent price action, our portfolios’ equity exposure had drifted down compared to our target weights and we have been acting to offset those drifts. As usual, we will be looking at the signals coming from our sentiment indicators before looking to make any material changes to our portfolios.

Markets react

USDRUB touched 90 overnight before fading back to the mid 80s - a record low. Global stocks tumbled, with the S&P 500 falling 2.50% at open, while havens and commodities surged. The flight to safety saw the 10-year Treasury yield touch 1.86% and gold hit the highest since early 2021. The dollar and yen jumped, while the euro and commodity currencies retreated. European natural gas soared as much as 41%, while WTI topped $100 and aluminum hit a record. Bitcoin slumped.

Impact on fixed income

Both Russia and Ukraine sovereign debt are facing sharp decline, down 30-40 points across the curve overnight. Russian credit is also wider by 20-30 points, depending on the name and credit quality. In the U.S., a seven-year Treasury auction is scheduled for this afternoon and many are expecting the highest seven-year yield since July 2019. Investment-grade credit is wider by five-to-seven basis points, with high-yield credit down 15-20 basis points, led by lower volume of 10%. Treasury flows are mixed.

What is causing equity markets to fall?

A combination of high inflation readings, hawkish comments from central banks and the events between Russia and Ukraine are causing equity markets to decline. In the United States, inflation is running at 7.5% - the highest level in 40 years - and markets now expect the Fed to lift interest rates six times this year. Amid the turbulence, however, it’s important to keep in mind that equity markets have climbed significantly since their March 2020 lows. Case-in-point: At its recent peak, the U.S. stock market had risen by 117%, while non-U.S. developed markets had gained 78%. These gains had been accompanied by signs of investor exuberance, evident in the crypto mania, meme stocks and SPACs (special purpose acquisition companies). Given all this, it’s not too surprising that markets have weakened.

Is concern over a larger market pullback warranted?

Financial markets tend to recover quickly from geopolitical events. The most obvious historical comparison, which was also the most significant in terms of market impact, is the Iraqi invasion of Kuwait in 1990. The S&P 500 Index fell 1.1% on the day, as the probability had been discounted by markets. The benchmark U.S. equity index would go on to decline by 16.9% over the course of 10 weeks, taking just over six months to recover. The key takeaway here: Stock markets can move past geopolitical events relatively quickly.

Historically, the main driver of whether we see a correction (a fall of, say, 10% to 15%) or even a mild bear market (with, say, a 20% decline that turns around relatively quickly) as opposed to a major bear market is whether there is a recession in the United States. In our view, recession risks, at least for the next 12 to 18 months, look relatively low. Strong household and corporate balance sheets leave us positive on the ability of the U.S. and global cycle to deliver significantly above-trend economic growth in 2022. Although the Fed is likely to begin lifting interest rates as soon as March, we believe it will take until at least the second half of next year for monetary policy to transition from being less stimulative to having a contractionary impact on the economy.

Key watchpoints amid the crisis

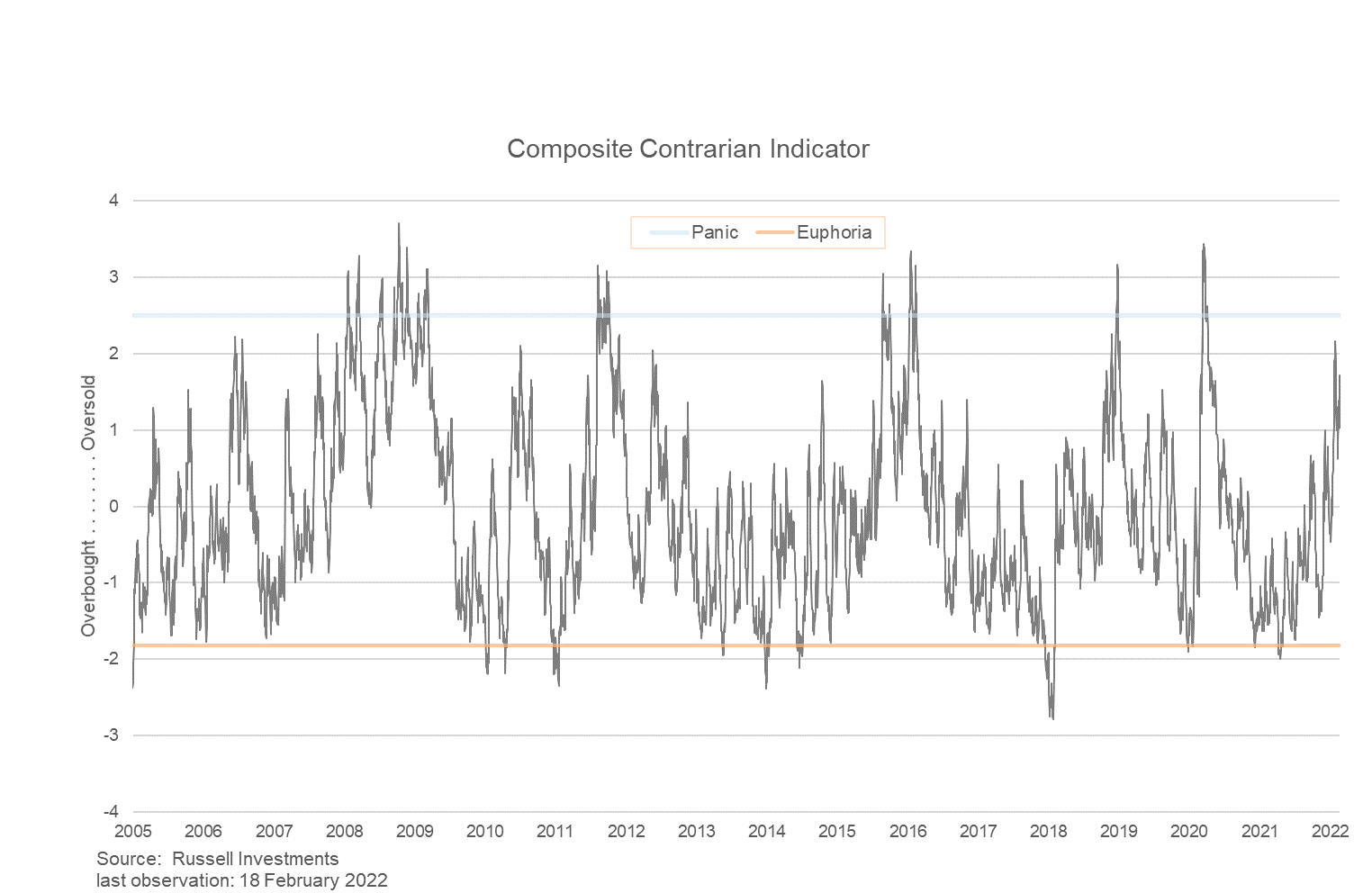

We evaluate potential market opportunities through the lens of our cycle, valuation and sentiment (CVS) decision-making process. We’re reasonably confident in the medium-term cycle outlook, and note that valuation has improved slightly as markets correct (although equity markets remain expensive from a long-term perspective). This makes sentiment the main watchpoint. Our composite sentiment index tracks technical, survey and positioning indicators to gauge whether investors are excessively optimistic or pessimistic. Sentiment has become oversold as markets have declined, although we believe it is not yet at a level of panic that provides a signal to add risk to portfolios.

We will monitor events in Ukraine closely, but with an eye on sentiment indicators to judge whether investor psychology has reached an unsustainable level of panic that justifies a more risk-on stance.

How are our emerging markets funds positioned?

Following the peak of the Russian market on 25 October 2021, the market as measured by the MSCI Russia Index has lost 35% of its value in USD terms as of 21 February 2022. Initially this was led by a severe pressure on the ruble, but as of today, the currency impacts are a bit less than previous selloffs with only eight percentage points of this selloff being currency-led. While Russia is a beneficiary of the high oil prices we have seen over this period, the escalation in tensions with Ukraine - and the question of whether or not President Putin will launch an invasion - is driving the negative sentiment. The threat of sanctions by the U.S. and European nations is putting further pressure on the Russian market today.

Our emerging markets funds have been overweight Russia throughout 2021, and generally benefited from this positioning as the market did well for the calendar year, despite the rising tensions from October onwards. We did see our Russia exposure decline toward the end of 2021, reflecting rising risks as well as profit-taking. The overweight in RIC PLC Emerging Markets Equity Fund has fluctuated between 183bps and 64bps active relative to the index throughout the past 12 months, and we are currently at 68bps active position (3.14% in the index as of 18 Feb 2022). The majority of our 3.8% exposure is through depositary receipts listed outside Russia - mainly in the UK. Our exposure to local listings is limited to 1.4%.

We have engaged actively with our managers on the Russian exposure throughout this period of heightened tensions, most of our GEM managers have maintained their overweight allocation to the Russian market this year, with many having reduced the bet toward the end of last year partly on profit-taking, as well as reflecting rising geopolitical risks. The current bet in our funds reflect the general view that despite all the noise in the market, a diplomatic agreement is more likely than a war with Ukraine. One manager is taking a different view, having reduced their exposure to underweight and seeing the most likely action to be entering and annexing the entirety of Ukraine for good.

Overall, the heightened sanctions risk is noted, though the expectation is also that no one wants to further disrupt energy prices. To be clear, this is a very evolving situation. We believe the Russian market remains attractively valued, as plenty of negative news has already been priced in, it offers attractive EPS (earnings-per-share) growth and a very high forward dividend yield for the market overall. This, in addition to a favourable economic backdrop of high oil prices and the fact a big portion of the market is dominated by dollar earners, gives comfort to our managers to take a more wait and see approach for now. This means not liquidating positions but equally not adding.

While there can easily be another significant leg down if there is a full-scale invasion, we believe there is also a strong upside risk in a no-full invasion scenario - and an even further upside risk with some sort of agreement. In our view, the Russian market has the potential to rebound very strongly if either of these outcomes pan out.

How are our global equities funds positioned?

Our World Equity Fund has no exposure, while our World Equity Fund II (WEF II) has 0.5% absolute or +0.2% active. We don’t see this as a direct issue for the funds. The broader comments above regarding taking a more wait and see approach for emerging markets equities are also applicable to WEF II. It’s only the two emerging markets specialists in WEF II (Oaktree, RWC) that have any exposure and they are roughly 1% overweight (or 4-4.5% absolute).

What are our specific views on the situation? How are they impacting our portfolio positioning?

We believe the changing risks of an invasion are reflected in market prices - hence the volatility we’re seeing now. And it goes without saying that we have no extra insight into President Putin’s mind, over and above the market, which - as we mentioned earlier - is relatively efficient at pricing these events. Our investment decisions are always driven by our cycle, valuation and sentiment indicators, which tend to ignore geopolitical noise. Importantly, our diversified, multi-asset investment portfolios are designed to deliver returns over the long term - and by design, will have exposure to multiple asset classes that will react differently.

For example, the fixed income exposure within our portfolios - particularly government bonds - typically increases in value during times of stress. We believe that this, alongside other defensive asset classes (such as gold, the Japanese yen or the U.S. dollar) should help offset some of the impact from equity moves. It’s important to understand that shorter-term volatility, while worrying, is normal when investing.

We are currently assessing the market’s reaction to the latest events and could be looking at some opportunities to selectively add to risk assets should our sentiment indicators point towards this direction.

What is our portfolio exposure to Russia and Ukraine?

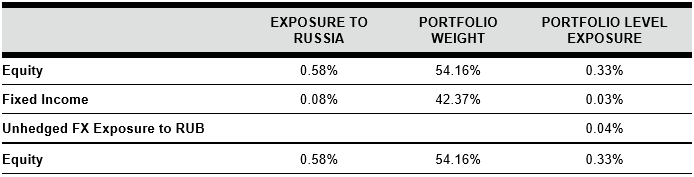

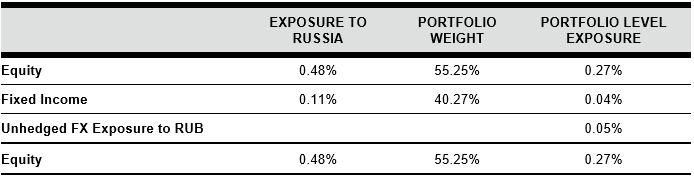

As you would expect from a highly diversified portfolio, there is some exposure to Russia and Ukraine within our portfolios, although it is not material. The table below shows the total exposure across Multi-asset Growth Strategy (MAGS) portfolios to Russia and Ukraine as at 17th February 2022.

MAGS GBP

Source: Russell Investments as at 17 February 2022.

MAGS EUR

There were no reported exposures to Ukraine in either portfolio.

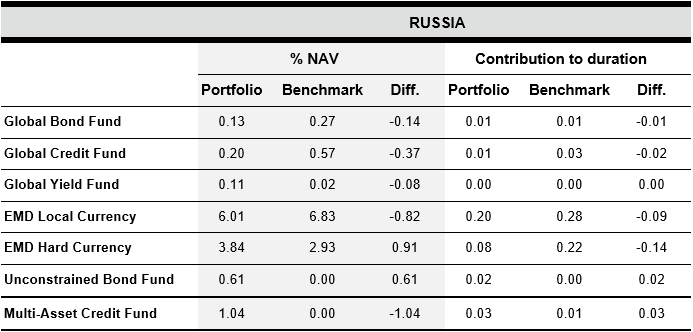

Fixed income

Overall, our fixed income exposure to Russia remains very limited, with most funds underweighting the risk versus its relevant benchmark, including our Global High Fund and Global Credit Fund. Our Global High Yield has a slight overweight of 0.08% in notional while it’s flat in risk terms, and our Emerging Market Debt Hard Currency has an overweight of 0.91% in notional, but underweights the index by 0.14yr in duration. Our Unconstrained Bond Fund and Multi-asset Credit Fund have a slight exposure of 0.61% and 1.04%, respectively, which translate into an active duration of 0.02yr and 0.03yr only.

Please see below our exposure to Russian assets within the different fixed income funds in absolute and relative to benchmark exposure as at 17th February 2022.

Source: Russell Investments as at 17 February 2022.

Important information

FOR PROFESSIONAL CLIENTS ONLY

This is not a marketing document. Unless otherwise specified, Russell Investments is the source of all data. All information contained in this material is current at the time of issue and, to the best of our knowledge, accurate. Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

The value of investments and the income from them can fall as well as rise and is not guaranteed. You may not get back the amount originally invested.

In the EU this document has been issued by Russell Investments Ireland Limited. Company No. 213659. Registered in Ireland with registered office at: 78 Sir John Rogerson’s Quay, Dublin 2, Ireland. Authorised and regulated by the Central Bank of Ireland. In the UK this marketing document has been issued by Russell Investments Limited. Company No. 02086230. Registered in England and Wales with registered office at: Rex House, 10 Regent Street, London SW1Y 4PE. Telephone +44 (0)20 7024 6000. Authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN. In the Middle East this marketing document has been issued by Russell Investments Limited a Dubai International Financial Centre company which is regulated by the Dubai Financial Services Authority at: Office 4, Level 1, Gate Village Building 3, DIFC, PO Box 506591, Dubai UAE. Telephone +971 4 578 7097.This material should only be marketed towards Professional Clients as defined by the DFSA.

KvK number 67296386

© 1995-2022 Russell Investments Group, LLC. All rights reserved