Municipal bond outlook – Hanging tough

Fundamental and technical factors driving resilience

With the extended May 17 U.S. tax deadline fast approaching, now is an appropriate time to take stock of how the U.S. municipal bond (muni) market has fared so far this year, and what we think could happen in the months ahead.

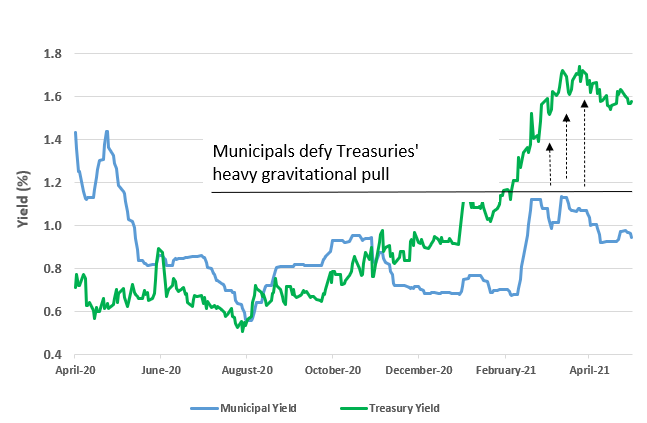

As we discussed in our last post, in late February, munis became too expensive compared to U.S. Treasury bills and sold off sharply, with muni yields spiking. A few months later, however, as U.S. Treasury yields continued their upward path (with their prices falling) due to rising inflation expectations, muni yields hung tough and prices remained firm on strong investor demand (see Figure 1 below). This meant that while the investment grade taxable bond market (as measured by the Bloomberg U.S. Aggregate Index) booked a -2.3% decline in the year to May 7, municipals (as measured by the Bloomberg Municipal Bond Index) returned 0.7%. This is a very big difference. The sub-investment grade market tells a similar story, with the Bloomberg Municipal Bond High Yield Index’s 4.0% year-to-date return (as of May 7) reflecting a 1.8% excess over the Bloomberg U.S. Corporate High Yield Index return.

Figure 1: Muni yields hang tough

Click image to enlarge

Source: Bloomberg, April 7, 2020 - May 7, 2021

While it may not be reasonable to expect munis to similarly outperform their taxable counterparts in the months ahead, they may still be able to resist (to a degree) further Treasury yield increases. Here’s why:

- Supply technicals: Approximately 3.5% of the municipal market is set to mature and be called through August, taking out supply. During this period the issuance may well be an amount less than that, creating what’s called net negative supply, meaning a shrinking supply of munis to buy.

- Demand technicals: Expectations of rising tax rates have kept muni demand robust, despite low yields. This should continue, driven by political uncertainty as the U.S. Congress wrangles its way through approving what could be trillions more in fiscal stimulus. Forthcoming stimulus could include a taxable municipal program similar to the 2009 Build America Bonds (or BABs) program, which might crowd out (or reduce) tax exempt bond issuance. The BABs program caused a tremendous number of foreign buyers to enter the U.S. municipal market.

- Credit quality fundamentals: High yield municipal defaults are expected to be a modest 2% of the outstanding bond market over the next 12 months (versus scarier double-digit forecasts from last year).Bolstering this is the recent trend of rating agencies issuing more upgrades and positive outlook revisions versus downgrades and negative watch outlooks. The CARES Act funding bolstered what in hindsight we can see was the pandemic’s only moderate effect on municipal finances. States and localities are now set to receive $350 billion from the American Rescue Plan to be put toward economic recovery efforts such as rehiring workers and supporting hard-hit industries.

The bottom line

Municipal yields (along with their performance) are still influenced by the direction of U.S. Treasury yields. A surge in U.S. government yields above 2% will surely drag municipal yields along. However, just as our tax deadline has been extended this year, it’s reasonable to expect any selloff in munis to be delayed over the next several months given compelling technical and fundamental factors.