Private Markets Outlook: A new world in 2023 and beyond?

As we look towards the new year, secular trends are occurring across global markets which will have profound impacts on the demand for private capital and for manager selection across private equity, venture capital, real estate, infrastructure as well as private credit strategies.

The COVID-19 pandemic only accelerated emergent trends promoting both regionalization and localization,1 two forces we see adding enormous opportunity for private market investment in 2023 and beyond. For example, substantial capital requirements and increased cost will be incurred to position more production strategically closer to consumption. In tandem, country of origin will be increasingly relevant to private market strategy development, especially as supply-side challenges are addressed via the private and public sectors. As such, we believe investors in private equity, venture capital, real assets (e.g., real estate and infrastructure), and private credit are positioned to take advantage with flexible strategies which are very much the domain of the local market. The result? A new world under development where the value of active ownership, local market expertise and global multi-asset relative value views will grow meaningfully.

What is the longer-term impact to private investment strategy development?

One potential by-product is markets becoming more asynchronous (e.g., lower correlations with other markets) based on the competitive positioning of a given country. Lower correlations will enable investors to benefit further from local market views and specialization. This global lens will be important as we see the expansion of the private market opportunity set into more regions for institutional investors, especially alongside government support and more innovative bilateral partnerships. For instance, the Inflation Reduction Act ("IRA") in the United States, while criticized for being protectionist, is just one example where a tax credit mechanism effectively ties the future of domestic electric vehicle ("EV") sales to investments into new mineral supply chains across North America and amongst U.S. allies. The construct of this type of policy is important as many nations, notably the U.S., want to be viewed much more as an investment partner versus solely a security partner.2 The endgame is we see more jurisdictions, particularly those supporting or progressing the benefits of private ownership, rule of law, and effective ESG characteristics positioned to compete for capital this cycle.

The reduction in business cycle volatility3 experienced over a multi-decade period and the attendant stability in interest rates as well as currency are in the rear-view mirror. The subsequent value of currency management and total portfolio exposure to the U.S. dollar ("USD") versus non-USD will be decisive factors driving return this decade. This is relevant as most private market strategies have benefitted as of late from a historic move in the greenback. Moreover, with the advent of distributed ledger technologies, a competition to effectively be the digital regulator of the world has already been underway. While governments will be actively involved in this process, much of this future will be funded via private markets, changing where as well as how things get financed. In the U.S., for example, legislation is needed to allow industries related to blockchain or even Web 3.0 to grow. Rep. Patrick McHenry (R – NC) on the U.S. House Financial Services Committee will be one to watch here in 2023.

We also believe the cyclical tension between ESG regulation and fiduciary implementation will grow. Importantly, global investors able to navigate these tensions correctly will have a large advantage. This tension is being tested in real-time via the Russian invasion of Ukraine and the energy crisis in Europe. This crisis is expected to endure at least through the winter of 2023, placing the future of German industrial and chemical production reliably in doubt. There is also a well-known supply problem with critical minerals required to support energy transition. Significant private investment will be required in sustainable mining and natural resource development which will take time. In our view, this highlights the caution needed around ESG being viewed as a negative screen;4 although, within private markets, the 'S' and the 'G' are table stakes. The importance of the social contract5 to operate and rule of law as well as governance will grow in this new world.

Ultimately, we believe private investment as well as the ability to control or influence performance of assets will play an even larger role in funding and building the future. While a global arsenal of capital has already been accumulating, funding remains modest relative to annual mergers and acquisition ("M&A") volumes or outstanding public market capitalization.6 Any pullback in capital markets will mean more opportunity for private investment strategies. Conversely, scrutiny around general partner (GP) skill as well as divergence between winners and losers will also grow. This divergence should usher in what could become a golden era of selection, particularly for those with advantaged access to broad ecosystems of investment opportunity alongside well-aligned partners.

What does this mean for private investments in 2023 and beyond?

As noted in prior outlooks, we believe private investments can be considered strategies focused on building, buying and using ownership rights to actively manage outcomes (e.g., active ownership). As such, an assessment of what should be bought and what should be built is continually relevant. For the first time in a long while, the market will be offering more opportunities to buy for institutional and retail investors alike, especially as the U.S. Federal Reserve seeks to disrupt demand without destroying economic activity. However, M&A and consolidation efforts do not existentially create new supply, requiring CapEx and development to be funded. With these considerations in mind, below are comments by key segments of private capital to help keep discussions going:

VENTURE CAPITAL

First the good news: so-called FOMO (fear of missing out) is dead, allowing cooler heads to prevail, especially as it relates to valuations. Venture capitalists did a good job pre-2022 accelerating exit opportunities and aggressively raising funds, including opportunity funds, to be able to position capital with their best performing portfolio companies across cycle. We will begin to see how this starts taking shape in 2023. The bad news: Headlines in 2023 and beyond will involve runway and down rounds.7

While labor policies worldwide and varying work visa rules will influence the flow of talent, we believe labor supply and wage pressures will serve as added catalysts for substitution of labor for capital (e.g., digitization and automation).8 For example, the power of conversational artificial intelligence ("AI") and regenerative models to process data at the periphery of networks (e.g., edge computing) will ripple through service industries starting this decade, unleashing productivity and improving the ability for small enterprises to compete profitably at scale.

For investors who ventured into places like South and East Asia to fund early-stage growth and forgot good governance was part of fiduciary duty, we think they will also experience selective pain in 2023 and beyond. Ultimately, for new investors, the investment period is your new best friend, offering potential extended periods to dollar cost average into category-leading companies. For existing investors, those with low legacy assets and high dry powder will be in pole position to win this next cycle.

PRIVATE EQUITY

Within control-equity transactions, dry powder remains at elevated levels while rising debt costs and tightening financing conditions can temper M&A volumes. This said, we often hear from GPs that unspent M&A budgets from 2022 will be a story in 2023, helping to produce exits. Any valuation gap between public and slower-moving private company valuations will imply a healthy uptick in taking publicly traded companies private as well.

Across the globe, much of the consolidation across a range of industries has taken place during a different regime, an attribute we anticipate will lead to higher non-core asset sales and corporate carveout opportunities. As an example, we see a related burgeoning market opportunity in Japan where the need to fund a domestic partner is high and the number of competitors is relatively low. We also see this opportunity set expanding in the UK as well as continental Europe.

With respect to distressed assets, we see high potential for the start of increased restructuring activity, especially amongst more cyclical businesses acquired at high valuations. However, we caution value in this market could simply mean high CapEx in disguise. While an elongated period of low interest rates and allowance for financial engineering (e.g., dividend recapitalizations, etc.) has served capital owners well, different tactics will be required to drive high growth this cycle. This said, new categories of investment including robotics-as-a-service and additive manufacturing (e.g., 3D printing) will be increasingly available to the enterprise, enabling more reinvestment while cutting the size of capital outlays required to improve the economics of businesses.

Finally, within the secondary market, unless pricing expectations fall, only the highest quality GP-led deals are expected to get done. More broadly, whether driven by denominator effect9 or portfolio-related challenges, the demand for liquidity solutions will increase from here as well as the valuation discounts required to clear assets.

UNLISTED INFRASTRUCTURE

Most of the cash flows associated with private infrastructure-oriented strategies have inflation-linkages, a feature which will continue to drive investor attention. Specific categories continue to need private capital, including secure data themes (secular rise in traffic via mobile, IoT and cloud), defensible energy transition (global policy priorities) and transportation innovation (modes disrupted but not displaced). There is an ongoing need for quality upgrades and more supply in all these spheres, and governments as well as corporates will need to seek financial solutions as debt costs rise.

With respect to energy transition, this theme encompasses one of the most important secular areas for private capital mobilization. As the base material for the bulk of the world's industry and petrochemicals, energy impacts every economic sector and region around the world. However, the U.S. is only one of a handful of countries even positioned to be able to substitute mass fossil fuel usage at scale. Australia is another. This environment is imposing a more pragmatic debate, pairing energy transition with energy security. We believe this will add momentum for countries to take a more realist approach to accelerate movement toward a more stable and hopefully cleaner energy future.

As noted earlier, the IRA in the U.S. is just one example of a policy response, often touted as one of the most aggressive actions taken on climate to-date. The IRA is intended to supercharge energy transition and motivate innovation as well as infrastructure investment.9 The overriding goal is to prime the domestic U.S. market to bring down the utility-scale cost of the energy transition and shore up critical supply chains. Energy transition and de-risking the EV battery supply chain are significant areas for global private capital mobilization.

PRIVATE REAL ESTATE

In the most basic form, real estate returns are driven mostly by a bond-like income yield from rents based on contractual leases and capital appreciation linked to demand for space. This demand is correlated to economic growth. In 2023, the relative value between public and private real estate will continue to be a headline. Groups able to engage in opportunistic REIT purchasing strategies alongside core and non-core real estate allocations will be prepared to generate better outcomes. Absent a major drop in interest rates, an increase in capitalization rates ("cap rates") is expected, resulting in accelerated capital depreciation across sectors. Complicating matters will be the need to actively repurpose space coupled with the barrier of higher costs. This means more CapEx budget and tech spend will be needed for business plans, promoting growth of markets including proptech.10

Irrespective of cycle, real estate strategies are very much a story about access to debt finance. The reality is widespread access to cheap debt tends to benefit sellers more than buyers. These dynamics have already started to change, creating a tailwind to real estate buyers; however, this will take time. Interestingly, retail assets in the U.S. are easier to finance than industrial properties today due to much higher cap rates, a feature which may start to unlock more attractively priced assets in 2023 and beyond.

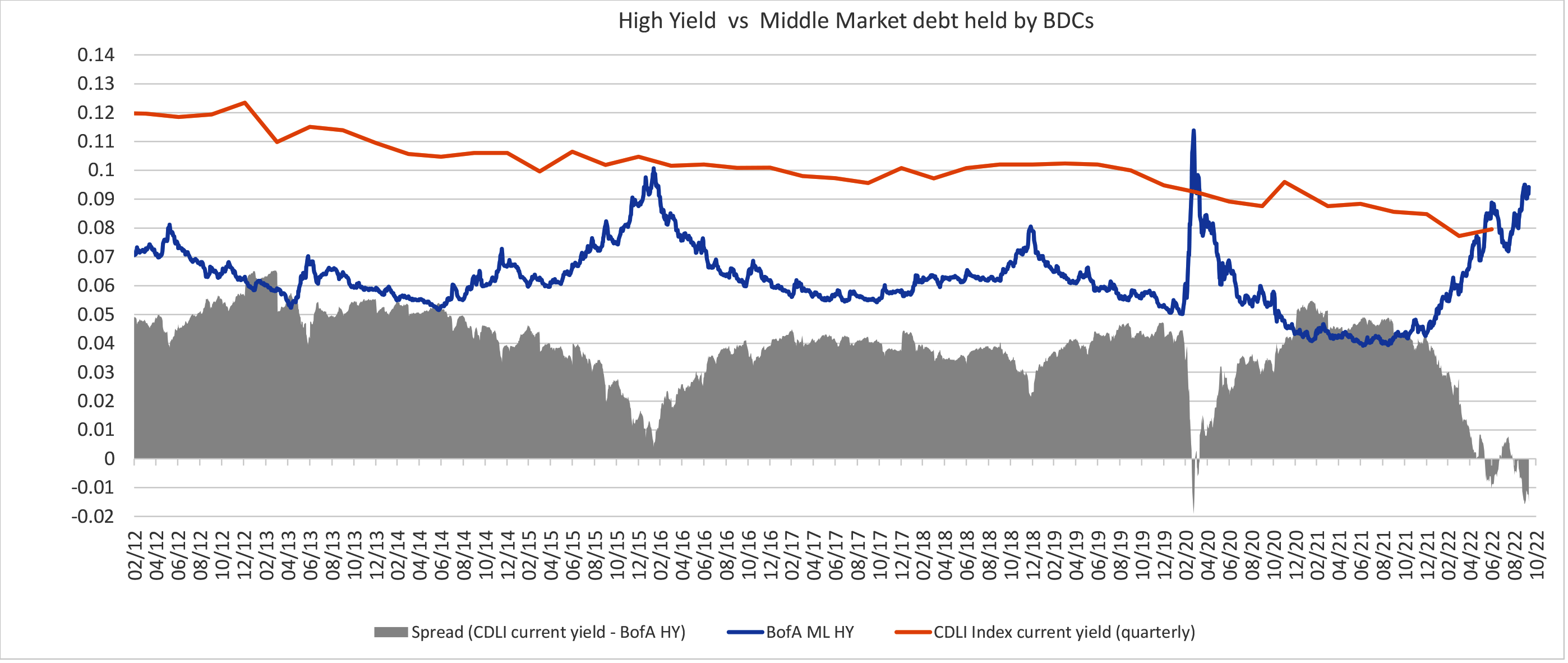

PRIVATE CREDIT

Following one of the most intense tightening cycles in modern history, the relative value between direct origination and broadly syndicated loans and bonds has narrowed. As higher capital costs translate to tighter fixed charge coverage ratios, leverage multiples have tightened as well.

Click image to enlarge

We expect elevated volatility to continue to transmit through currencies, rates and credit spreads in 2023. As such, we still see high investment proposition via opportunistic credit strategies with the ability to toggle relative value between cheaper public securities and direct origination. It’s worth a reminder, during the Global Financial Crisis, transaction volumes fell significantly in large part due to a lack of debt finance. With the advent of the non-bank market, we expect more of a floor behind transaction volumes this cycle but at much higher cost, benefitting direct originators.

We continue to see the need for high private investment to finance resilient supply chains, future-proof assets, and build what is needed in the future. For example, going back to the topic of energy, the largest source of capital required for energy transition will be credit. This highlights more of the future will be capital-intensive and potentially require the private sector to partner with governments more. Being on the right side of contemporary industrial and regulatory policies will be more important as a result. However, as credit is a contract, this only serves to reinforce the importance of rule of law, strong governance and ESG commitments as decisive tools involved in funding the future.

One final question: Who will benefit the most from free cash flow to the firm (FCFF) this cycle?

Investors are entering a world where CapEx, working capital, cost of debt and taxes are expected to trend upwards. Given the scale of challenges being confronted, there are more questions surrounding how equity in aggregate will generate the required return on equity this cycle. We believe selection spreads will widen considerably and investors will be paid more to be senior secured, where there is first dibs on free cash flow. Private credit specialists are emerging in almost every vertical to help enable sponsor and non-sponsored companies to thrive and create broad diversification in private credit portfolios. More broadly, we believe a global multi-asset investing approach informed by local market resources with an open-architecture platform to enable access to talent plus the full private investment opportunity set, will also be a winning hand in this new world.

1 Regionalization encompasses the shift of economic activity and bilateral / multilateral agreements into smaller economic units or regional groups, embracing regional ties and/or alliances as a means to succeed in an internationally competitive world. Regionalization acknowledges geographical constraints and the impact of differing political economies as well.

2 For example, it would not surprise us to see more institutional investors developing a Western Hemisphere strategy or funding strategies targeting sustainable growth and urbanization across the continent of Africa this decade.

3 The Great Moderation: https://en.wikipedia.org/wiki/Great_Moderation In-depth look: https://www.richmondfed.org/publications/research/goodfriend/hetzel

4 As it relates to decarbonization, a border-adjusted carbon tax, for example, is just one potential policy consideration investors should have on the radar this decade. A carbon tax, border-adjusted, works via sending price signals on carbon globally through the tax system to enable funding.

5 It's worth highlighting U.S. and Western countries are not immune. For example, entitlement reform in the U.S. and confidence in the government’s ability to adhere to promises made via programs such as Social Security, will be increasingly contested and more visible this decade, especially as the 2024 Presidential election cycle unfolds.

6 According to Pitchbook, the private market industry had $1.3 trillion in dry powder as of 3Q 2022 with well over half accumulated post-2019 vintage. This statement acknowledges the size of the non-bank lending market is now roughly equal to the size of leveraged loans and high yield markets.

7 Runway: How long a venture startup has before running out of cash and needs to raise another financing round. Down round: A financing round at a valuation less than the valuation marked during the prior round.

8 For example, in the U.S., there are 250k-300k quick-service restaurants with drive-through service. In the next five+ years, 250-300k jobs taking orders will actively be substituted with conversational AI tools. While the technology already exists, the proposition to invest is different when labor is $9/hour versus $19/hour.

9 Key to the IRA is ability for utilities to pay for energy transition through tax credits versus passing costs directly to consumers through higher rates.

10 Property Technology or proptech: https://en.wikipedia.org/wiki/Property_technology