Banking collapses and rate hikes unlikely to stall bond market recovery

Fixed income remains on track to record a better 2023 but investors who stay nimble in the continued market uncertainty will be best placed to maximise opportunities without taking on undue risk.

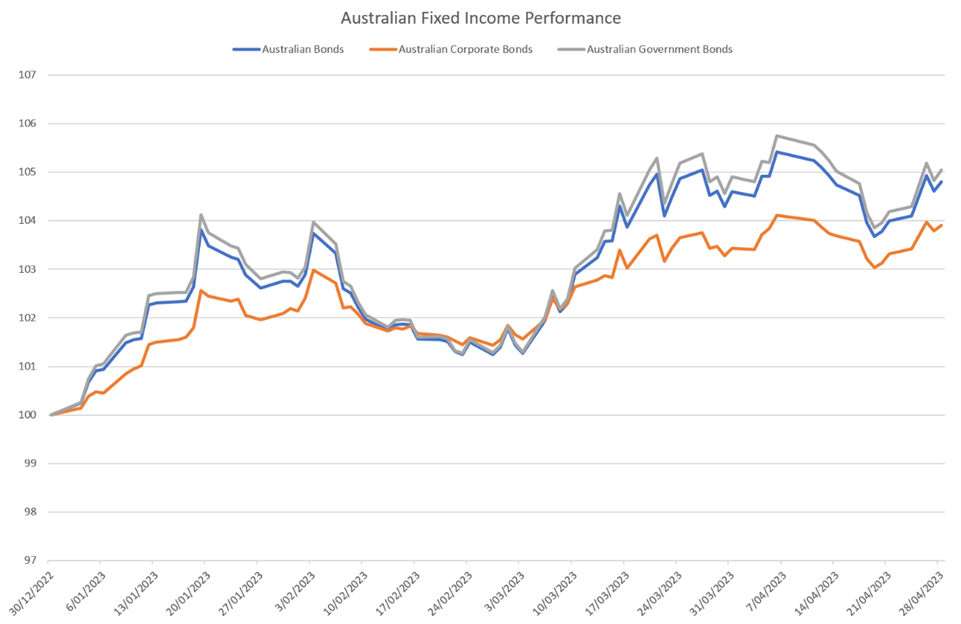

In the calendar year to April 30, the broad Australian fixed interest market – as measured by the Bloomberg Ausbond Composite Index – returned a healthy 4.8%.

Drilling down further into the asset class, government bonds gained just over 5% in the same period and the Bloomberg Ausbond Credit Index rose 3.9%. The relatively lower returns of corporate bonds are unsurprising as continued volatility has driven a preference for quality and duration within fixed income markets.

These solid gains were a welcome relief to advisers and their clients after the Bloomberg Ausbond Composite Index fell 9.7% in 2022, defying traditional wisdom that bonds should rise when equities fall to provide a ballast to portfolios.

There is a reasonably good chance that stronger returns will continue throughout the rest of 2023, though it’s unlikely the losses of last year will be entirely erased by year-end.

Click image to enlarge

Source: Russell Investments

Why this outlook?

There are several reasons for this outlook.

Unless economic data delivers surprises, cash rates appear close to peaking in most markets. It’s worth noting, though, that the probability of an actual reduction in official interest rates in Australia this year remains low.

Secondly, the US banking crisis is unlikely to have a last impact on the fixed income market. The biggest consequence of the crisis on all assets – including equities – was that it created more volatility and uncertainty for advisers to navigate.

Changes to take into consideration

In good news, two factors have offset this uncertainty to some degree. Number one, the crisis was very specific to a handful of companies in the US. And the market also quickly priced in the central bank reaction to the bank collapses that did occur.

Nonetheless, the crisis did signal changes to the outlook and macro environment that advisers would do well to take into consideration.

For example, the crisis provided an indirect signal there is more stress in the financial system than first thought after the rapid interest rate increases of the past 12 months. In other words, the potential impact of the hiking cycle wasn’t properly priced into the market.

Central banks may now be more cautious about the outlook in recognition of the stress and uncertainty in the system. For example, they may tread more carefully with interest rates, particularly in the US where it is not unreasonable to expect fewer rate hikes than previously anticipated. Any rate increases that do occur may also be more spaced out than those which occurred earlier in the cycle.

Remain nimble

In the remainder of 2023, it’s best to take a selective approach and remain nimble to capitalise on opportunities as they arise.

Exchange traded funds remain a good way for advisers to achieve this goal, particularly those which give access to the government bonds and investment-grade corporate debt that may benefit from a continued flight to quality in the sector.

In a world where large changes in cash rates and interest rates are unlikely, advisers should be able to add value by looking for higher yielding assets – this means higher quality, or even shorter dated, parts of the credit market.

Investors who are willing to shift between credit risk and duration in government bonds and investment grade corporate bonds may be best placed to take advantage of volatility as it occurs.

The aim of advisers should be to deliver the best yield possible for clients – without taking too much risk by blindly chasing returns.