ETF Investing in troubled times

Equity market leadership has seen some material changes in 2022 driven by the conflict in Ukraine. In the year to 31 October, the Energy sector in Australia returned over 50%1 having lagged for much of the previous decade. Changes of this magnitude have challenged some equity strategies, particularly those with an ESG objective.

Russell Investments two equity ETFs, Russell Investments High Dividend Australian Shares Fund (RDV) and Russell Investments Australian Responsible Investment Fund (RARI), were both reconstituted on 30 September 2022 to reflect the latest data from the August reporting season. In this blog, we discuss the key changes to the ETF portfolios and factors behind the moves, along with their recent performance.

RDV – Russell Investments High Dividend Australian Shares ETF

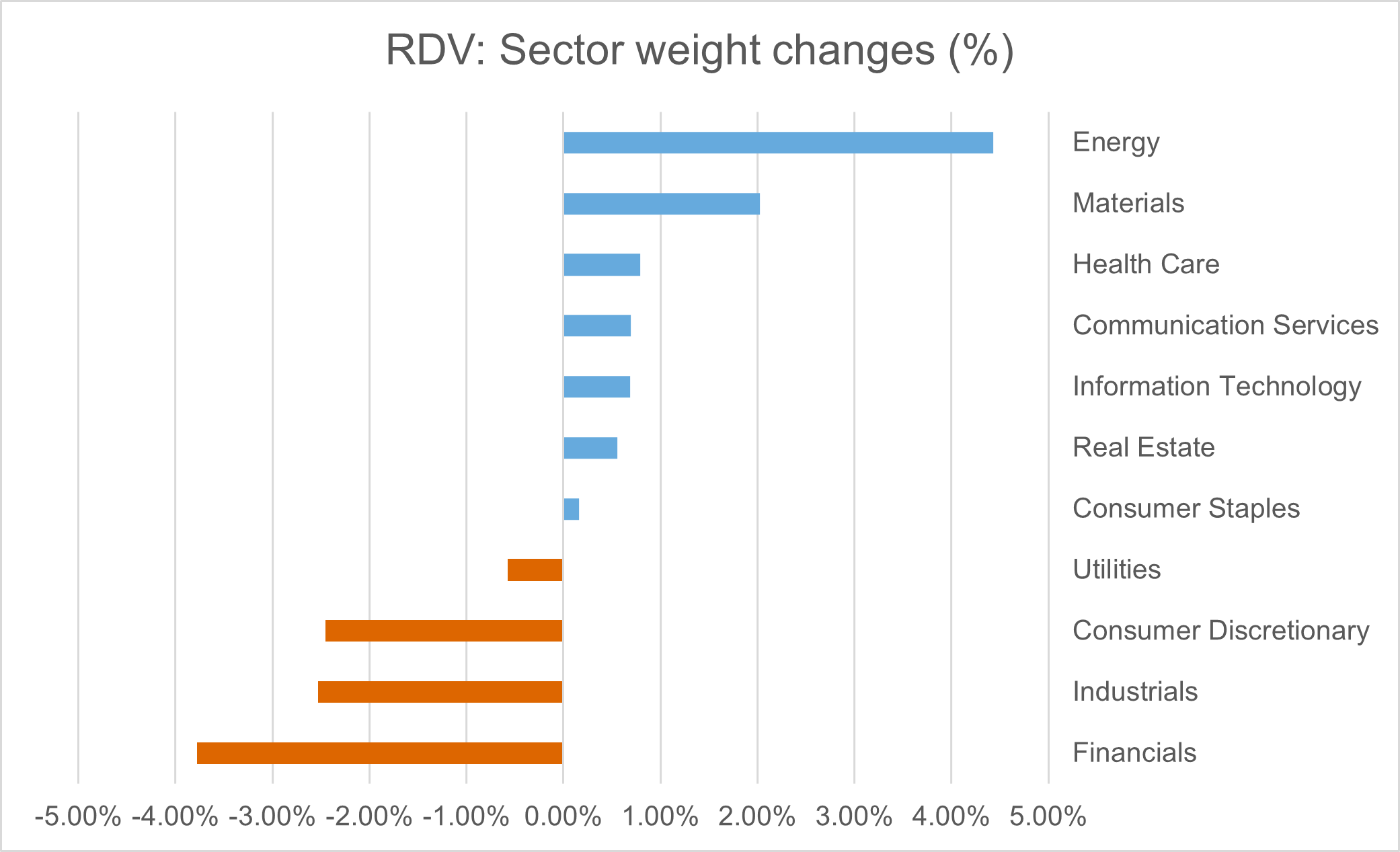

Investors in RDV were paid a healthy 2% (55.2c) dividend in October for the Q3 distribution, reflecting a solid reporting season and strong dividends – particularly from the Energy and Materials sectors. Soaring energy prices have boosted the earnings of many commodity-based stocks and as a result, index heavyweights like Woodside Energy Group and BHP are sitting on 1-year historic dividends approaching double digit yields. It is therefore no surprise that the biggest weight increases at the reconstitution were the Materials and Energy sectors.

Source: Russell Investments. Sector weight changes from previous reconstitution on 31 March 2022 to 30 September 2022.

At the stock level, 7 new stocks were added with Whitehaven Coal the largest new buy at a 3% weight. The energy crisis in Europe has resulted in coal prices surging, boosting Whitehaven’s earnings and dividend expectations. In addition, Whitehaven recently announced an on-market share buy-back program, which will further support the stock price in the short-term. Santos was another new buy in the Energy sector. Its dividend credentials were supported by rising oil and gas prices.

The funding for the new RDV buys was from the Financial sector, with the portfolio selling out of Macquarie group. Despite the 3.8% reduction to Financials at the reconstitution, RDV remains overweight to the sector versus the S&P/ASX 200 Index since most banks and insurers continue to offer attractive fully franked dividends.

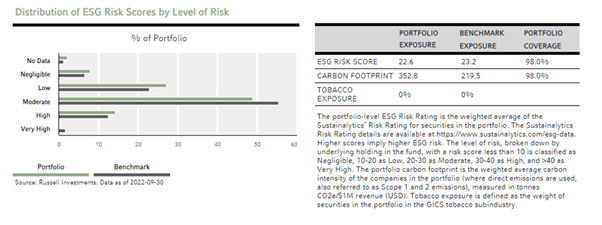

RDV’s index methodology does not include specific ESG objectives and the move into fossil fuel related mining stocks reflects their dividend credentials in the current economic climate. As a result, RDV’s carbon footprint has jumped following the reconstitution, however, the Sustainalytics ESG ‘risk score’ of the portfolio remains below benchmark as shown below.

Source: Russell Investments as at 30 September 2022. Portfolio Exposure reflects RDV’s holdings, whilst Benchmark Exposure is the S&P/ASX 200 index

RARI – Russell Investments Australian Responsible Investment ETF

ESG strategies have struggled during 2022, however RARI has outperformed many of its peers from a ‘Value’ exposure embedded in the portfolio construction methodology. RARI uses dividend characteristics and ESG scores to select stocks. This results in a portfolio with an overweight to Financials and some holdings in the Materials sector, both of which provide exposure to the ‘Value’ factor.

RARI has a broad ESG exclusions policy, and the fossil fuels screen means the portfolio does not currently hold any Energy stocks. However, despite this RARI has only lagged the benchmark by 1.9% in the first 10 months of 2022. This compares favourably to most other ESG Australian shares ETFs, some of which have underperformed the benchmark by as much as 10%2 in 2022.

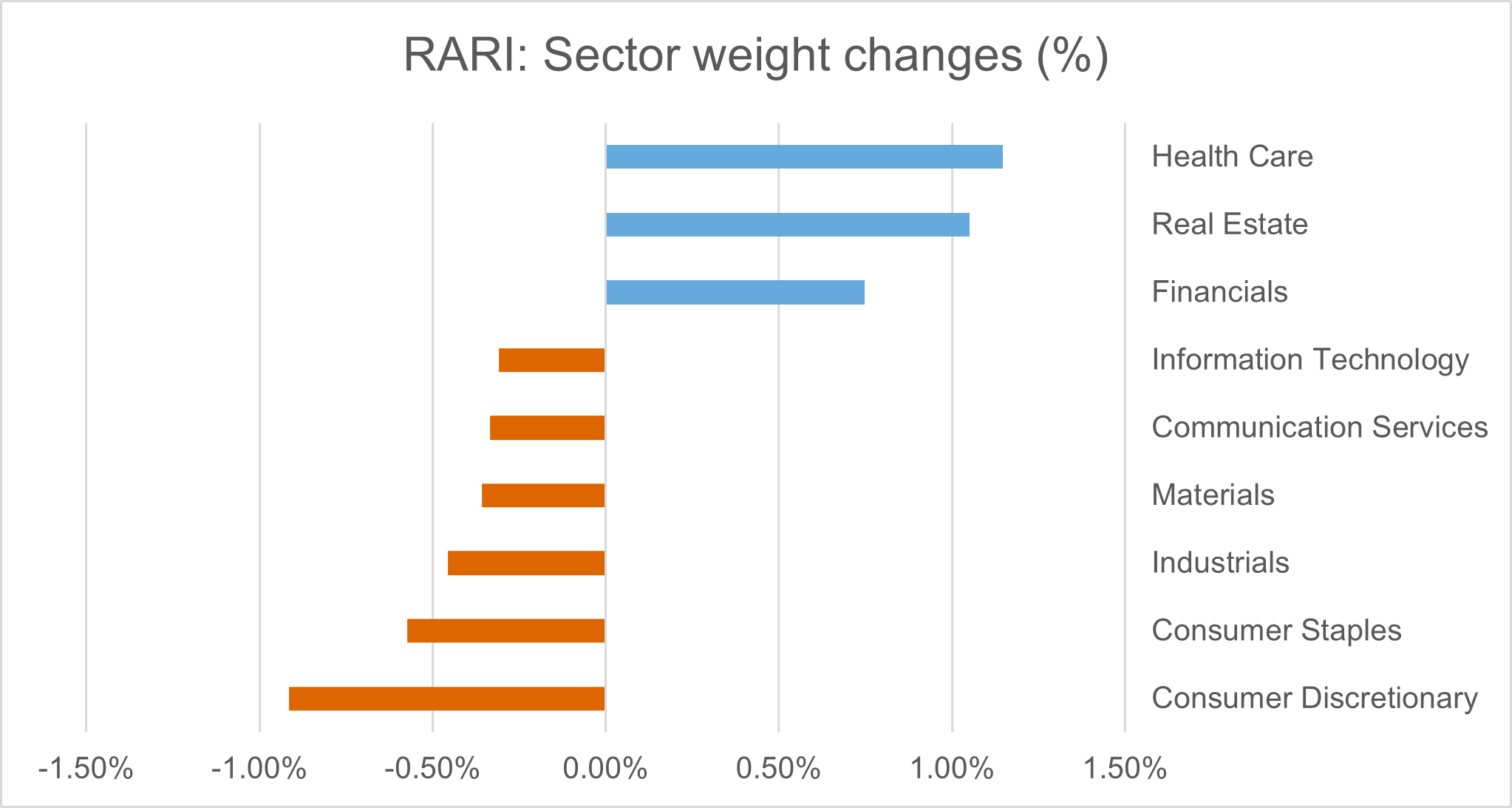

RARI’s portfolio construction process does permit exposure to mining companies not exposed to fossil fuels, with holdings in IGO Ltd and Oz Minerals which added incremental returns in Q3 2022. IGO extracts metals essential for a clean energy future, such as lithium required for electric vehicles, and RARI is overweight this stock versus the S&P/ASX 200 Index. Similarly, an overweight to Oz Minerals due to the company rating well on our Material ESG scoring methodology also boosted RARI’s performance. Oz Minerals focuses on copper and its share price jumped thanks to a bid from BHP. Both stocks saw their weights trimmed at the reconstitution due to substantial outperformance, reducing their overall dividend yields:

Source: Russell Investments. Sector weight changes from previous reconstitution on 31 March 2022 to 30 September 2022.

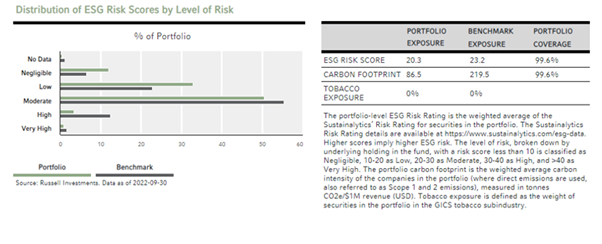

RARI’s reconstitution was more modest than RDV’s. The portfolio turnover was only 10% compared to 16% for RDV. The largest weight change at the sector level was a 1.2% weight increase to Health Care. CSL’s weight rose by 0.5% and Sonic Healthcare by 0.7% driven by strong Material ESG scores and an attractive fully franked dividend in the case of Sonic. As to be expected, RARI’s carbon footprint is well below benchmark, and it has markedly better ESG scoring characteristics.

Source: Russell Investments as at 30 September 2022. Portfolio Exposure reflects RARI’s holdings, whilst Benchmark Exposure is the S&P/ASX 200 index.

RARI’s predicted tracking error is 4.2%, relatively low compared to many other ESG strategies and a good outcome given the superior ESG characteristics when compared to the S&P/ASX 200 index above.

The importance of risk management

This year has been a reminder that risk management is important if investors wish to avoid large drawdowns versus market benchmarks like the S&P/ASX 200 index. It appears we are set for choppy markets for the foreseeable future, given inflationary pressures mean we cannot expect to return to a low interest rate environment that we had become accustomed to. This has implications for equity strategies, and we continue to believe the benchmark relative approach used for RARI’s portfolio construction will help ESG based investors navigate these volatile times.

1 Bloomberg

2 Bloomberg and Russell Investments

This article was produced on 7 November 2022 and views expressed may have changed. Readers should consider viewing more up to date material on this topic.