Problems of plenty: Can active managers manage their AUM?

Toward that end, we have our own sets of preferences which we believe contribute to active manager outperformance. And it’s no secret that, when it comes to active managers, one preference we have is for managers with a relatively small amount of assets under management (AUM). The reasoning behind this is a combination of science (in the form of 15 years of data and in-depth analysis) and art (in the form of face-to-face meetings and assessing multiple more nuanced factors). We still believe small-AUM managers tend to outperform. Less AUM to manage means, in the simplest terms, more nimbleness when it comes to finding upside opportunities and managing against uncompensated risk. This is especially true in portfolios with liquidity constraints.

But our data also shows us that increasing AUM is not necessarily the kiss of death. As AUM increases, we typically see active managers increase the number of holdings, reduce their active share, reduce turnover, and move toward more liquid stocks. What we believe determines the performance, then, becomes the managers’ skill in doing these things well. And, by looking beyond the data, we do find managers who can do these things well.

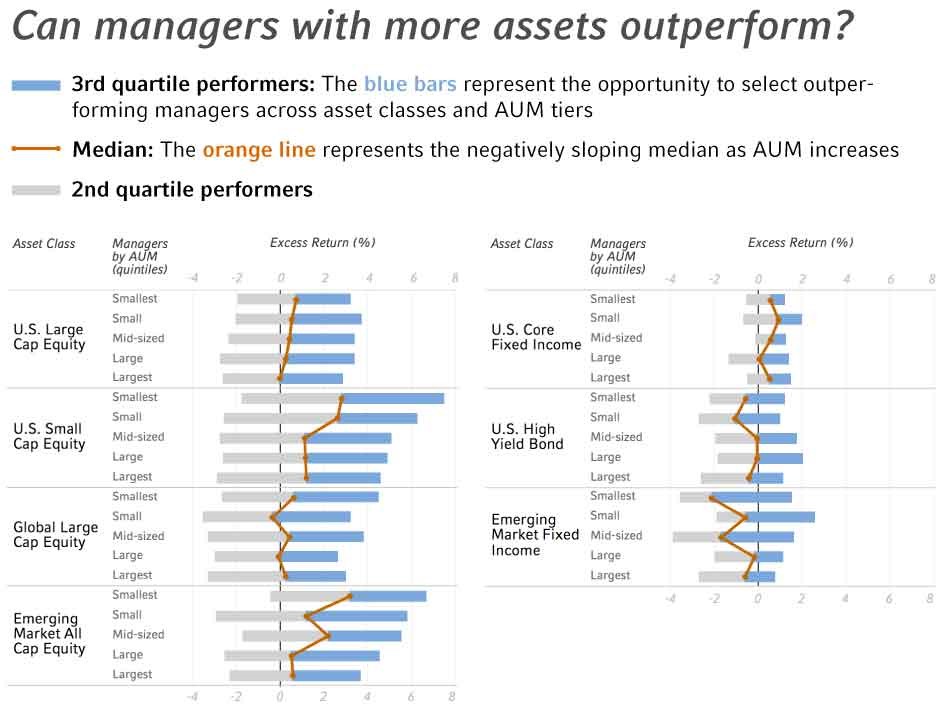

When looking across the AUM spectrum, we find that even some active managers with more AUM are able to generate strong performance. In the case of equity, we find the size effect is strongest for U.S. small cap and emerging markets equity where, as investors would expect, liquidity is more of an issue. Yet even in the U.S. small cap space, we find that increasing AUM is not as strong a detractor as it was 15 years ago when we did our first study.

Below we have charts that exhibit the interquartile ranges of one-year returns (2001-2015), broken out by AUM quintiles, for active managers across various equity regions and fixed income strategies. While we observe a (mostly) downward trend for the range of excess returns as AUM increases in the equity regions, the 75th percentile manager excess returns are positive and the medians are mostly positive. In the case of fixed income, a trend is not so clear. Yet, in the case of fixed income strategies, we also observe the strong upside at the 75th percentile.

Source: Russell Investments. These are based on observations from products in Russell Investments’ active manager universes. The average number of products per period ranges from approximately 50 to 300 by region.

Given this and other Russell Investments research1, we have confidence that managers whose AUM has grown may be worth keeping—within limits. As we know, past performance is not indicative of future results. But we see a similar upside of returns among larger AUM managers to what we have observed in smaller AUM managers. In other words, some managers manage their AUM growth well. Some don’t. And simple metrics are insufficient for evaluating which active managers can do so.

We also believe there are limits to this. Ultimately, we suspect that active managers do have limits to the AUM they can manage, but they may be self-regulating to stay within those limits. We’ll pick that up in a future blog post.

1 Research dating back to 2001. Christopherson, Jon, Zhuanxin Ding, and Paul Greenwood. "The Perils of Success: The Impact of Asset Growth on Small-Capitalisation Investment Manager Performance." Research Commentary, July 31, 2001.