RBA follow through on their threat

The Reserve Bank of Australia raised the cash rate to 4.35% at the November meeting. This follows the comments from the new RBA governor, Michelle Bullock, that the RBA would not tolerate upside risk to inflation and a slower return to the inflation target. The Q3 inflation print was higher than expected, and this appears to be the catalyst for today’s decision. Looking ahead, the RBA have softened their rhetoric around future rate hikes and appear to have become very data dependent now.

Let’s start with those inflation numbers. Core inflation in the third quarter came in at 1.2% quarter-on-quarter, compared to expectations of 1.1%. The inflationary pressure was quite concentrated, with rents, electricity and fuel accounting for the majority of the total inflation print. The RBA did not indicate in the statement how much this print has changed their forecast on the path back to the inflation target, but clearly it was enough of a shock.

More broadly, the economy has still not felt the full impact of the tightening that had occurred before today’s decision given some mortgages have not rolled off from very low fixed rates. That said, we have seen some signs of slowing that have already come through. We don’t think that today’s hike materially increases the risk of a sharper downturn – that risk would arise if we saw a number of rate hikes from here, which we think is unlikely.

The RBA’s key focuses have been on household consumption, the labour market and the international experience. Let’s go through the three of those.

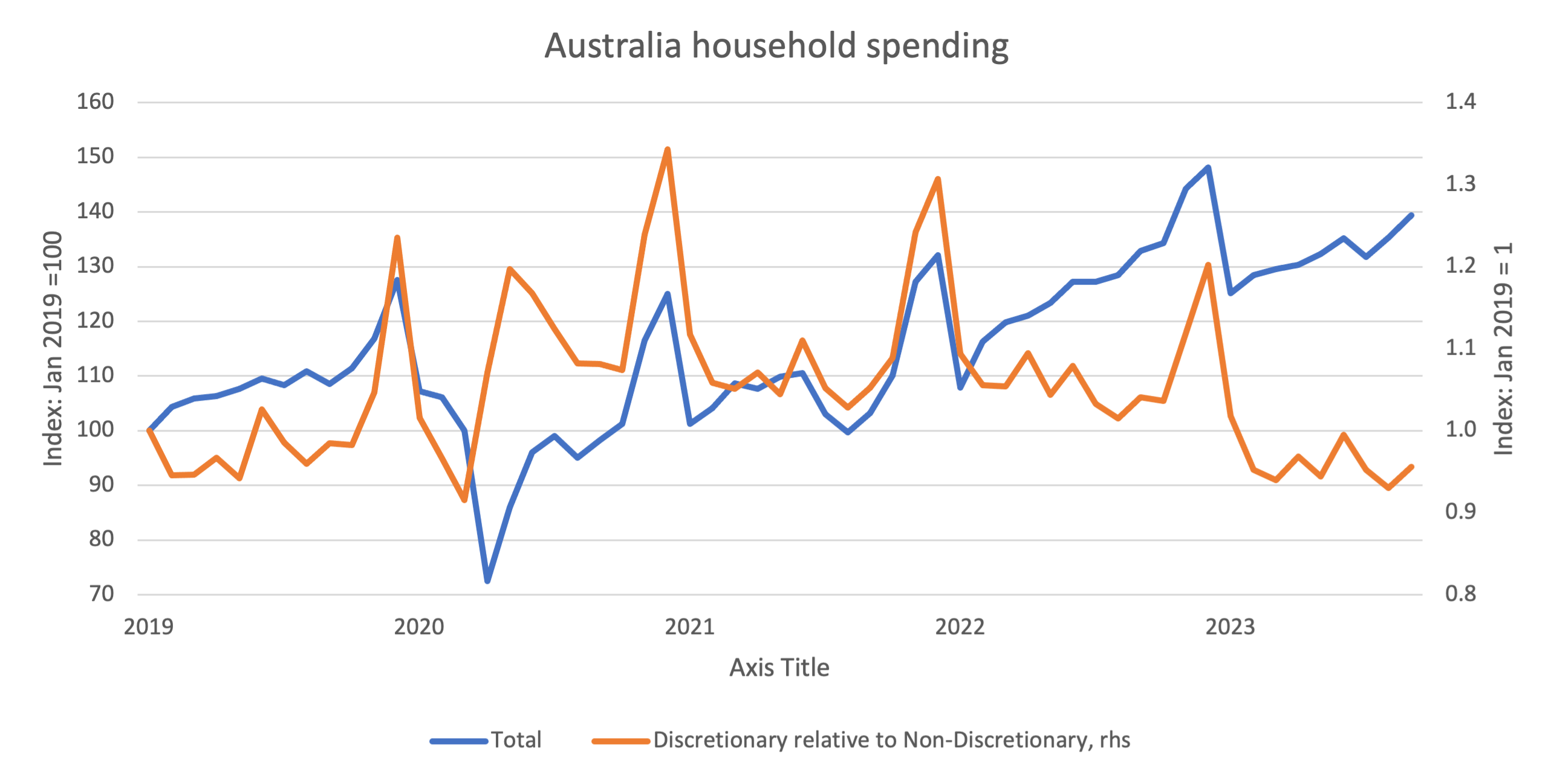

Household spending is holding up.. for now

Australia household spending has picked up in the last couple of months, although a lot of that has been in non-discretionary spending. If we zone in on retail sales, we similarly saw a pick up in volumes (i.e spending adjusted for inflation). However, that appears to be largely driven by discounting and unseasonal weather, and so is unlikely to indicate a resurgence in spending.

Source: Australian Bureau of Statistics, 3 November 2023

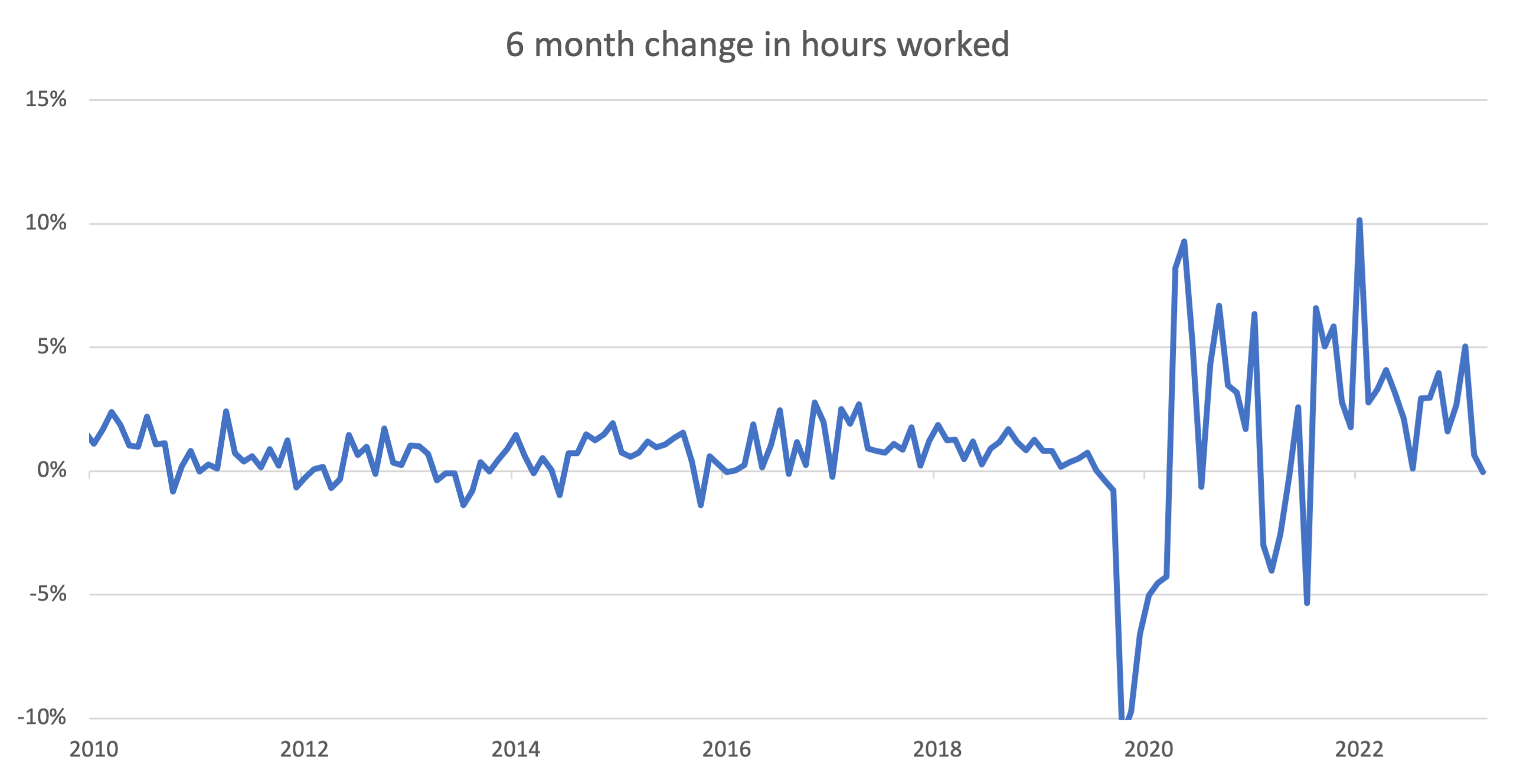

Hours worked has slowed

The headline jobs numbers have remained pretty robust, all things considered. However, under the hood we can see signs that it is slowing and the forward indicators suggest further slowing is coming. Rather than looking at jobs, it is beneficial to look at hours worked. As the economy accelerates or decelerates, employers are generally more likely to change the hours of their current staff than change the number of staff they have. This means that hours worked acts as a lead indicator for the broader labour market. Hours worked are now effectively unchanged over the last six months – so we have added more workers but there are less hours being worked in total. This is also leading to the underemployment rate – which captures people who are not working as much as they would like – to rise. This is important as over the last ten years, wage growth has been correlated more with the underemployment rate than the unemployment rate.

Source: LSEG Datastream, 7 November 2023

Globally, central banks have remained on hold

Finally, on international developments. Last week, we saw the US Federal Reserve and the Bank of England hold rates steady, albeit at much higher levels than we see in Australia. As highlighted here, we think that both central banks are likely finished in their hiking cycle.

Investment implications

We highlighted earlier that this rate increase doesn’t materially change our view for the economic outlook from here – we think Australia will continue to slow but has a lower risk of recession compared to developed peers in the northern hemisphere. But does it change our view on key Australian investments? Similarly, not really.

We continue to think that Australian government bonds are attractively valued and should provide diversification benefits if we hit a nastier growth environment. Indeed, just looking at today’s market action, Australian government bonds rallied on the news that the RBA had hiked.

We think that the Australian dollar is going to be volatile in the near term but have upside over the next twelve months. This rate rise, at the margin, helps the case for a higher AUD as it reduces the interest rate differential between Australia and the US.