Be the architect of your retirement income

It’s how you combine the basic building blocks of age pension, superannuation, and other savings that will determine what your retirement income looks like. The results will be unique to each person.

By Adam Krull - 3 min 30 sec read

A little about Adam

For nearly five years, Adam has been helping members of the Russell Investments Master Trust prepare for their retirement with confidence and peace of mind. With a career focussing on corporate super, finance and insurance, he offers clarity and support in the form of general information, so members can understand their options for a great life after work.

Look down any suburban street and you will see examples of how similar inputs can achieve different results. Every occupied house has walls; windows; doors; a roof. Each property is a home where people can live. But it’s how these elements are combined that determines who that property suits – a busy young family, a single businessperson, or a couple of active retirees, for example.

Preparing your retirement income is a bit like building a home. You have a limited range of components to work with – superannuation, the Government Age Pension and other investments, rather than windows and walls – but how you construct your retirement income will be unique to your individual needs.

Basic building blocks

Like different building materials, each source of retirement income has its uses and limitations.

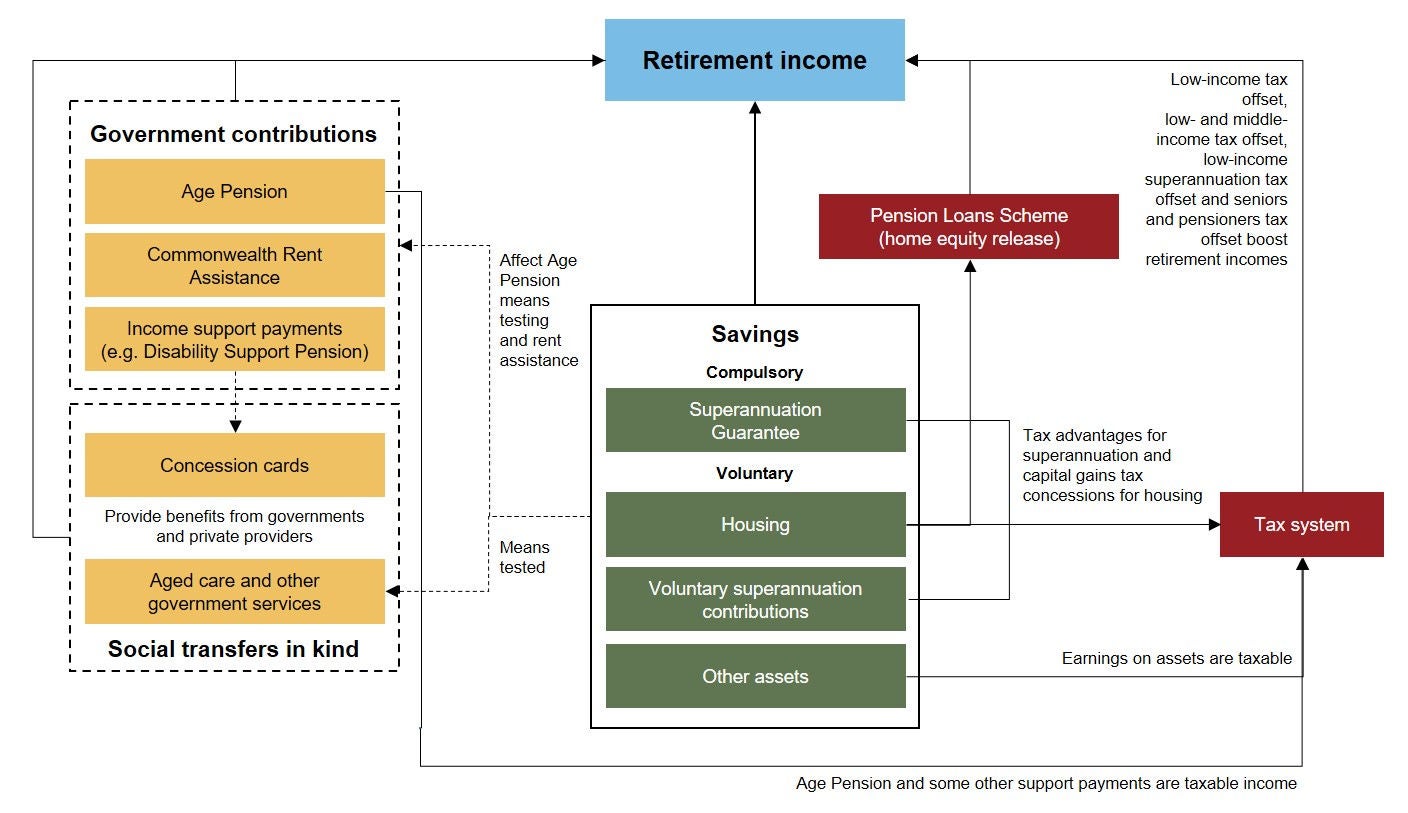

The chart below from Treasury’s Retirement Income Review in 2020 shows the key elements that can make up a retirement income.

Key retirement income sources

Source: Based on The Australian Government the Treasury data in the Retirement Income Review Final Report, July 2020, p.68

Support for security

Government contributions such as the Age Pension provide income support to retired Australians who need it. Think of this as your back-up protection, like fire resistant shutters or raised floors in flood-prone areas: not everybody needs it, but it’s invaluable if you do.

Whether you qualify to receive the Age Pension depends on your age, residency status, and level of income and assets. Read more about Age Pension eligibility.

Your super and savings – the additional trimmings

The savings you build up throughout your life will form the foundations and structure of your retirement income, as well as providing for any additional trimmings, ideally worthy of a Better Homes and Gardens front cover.

Most people will fund a large part of their retirement income from private savings. This includes superannuation guarantee savings you have accumulated through compulsory employer contributions into your super fund, voluntary contributions to super, housing and other investments outside super.

Superannuation is a highly tax effective way of building up savings to generate income in retirement. Contributions into super and earnings on investments held in your fund are usually taxed at 15 per cent rather than your marginal tax rate outside your super fund. After retirement, you generally pay no tax on earnings and capital gains on investments held inside super.

When you retire you can convert your super into an account-based pension or an allocated pension, which provides a regular, flexible and tax-effective income from your super. We can assist you on how to do this.

The limitation of super is that in general, you can only access your funds after you have met certain conditions, such as having permanently retired and reached what’s known as preservation age, which ranges from 55 years to 60 years, depending on your date of birth. Learn more in our When you can access your super fact sheet.

If you retire early, you might need to fund your retirement out of savings outside of super until you meet one of the conditions of release.

There are no restrictions on how you spend savings you have accumulated outside of super, but unlike super, there are no specific tax advantages.

Under construction

How you combine the basic building blocks available to you to construct your retirement income will depend on your own circumstances.

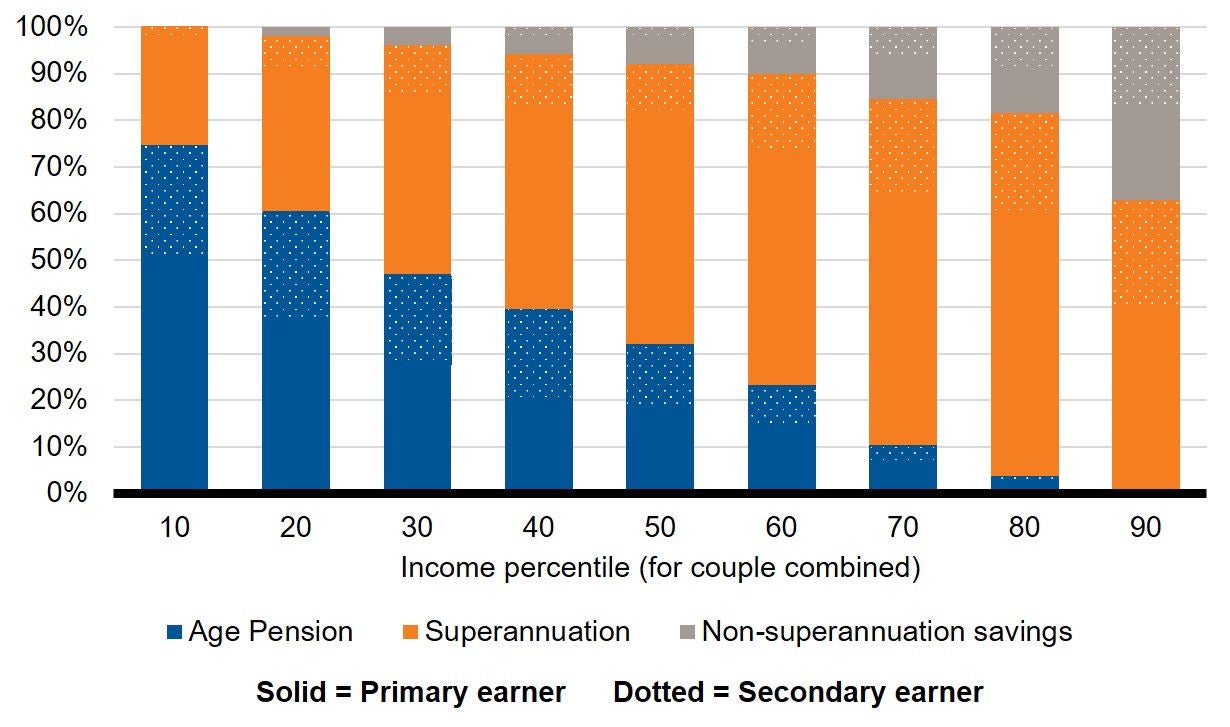

Higher income couples usually rely more on their super and non-super savings for income in retirement, while people in lower income brackets derive a higher proportion of their retirement income from the Age Pension. Chart 2 below from the Retirement Income Review shows the projected proportions of total retirement income for couples with varying income levels.

Proportional source of projected total retirement income for couples by percentile

Source: Based on The Australian Government the Treasury data in the Retirement Income Review Final Report, July 2020 (page 281)

To begin the process of planning for your own retirement income, you will need to understand the components you have got to work with. You will need to answer questions such as: How much do you have in super now, and outside your fund? How much can you expect to have at retirement? Is it likely you will receive the Age Pension?

Designing your retirement income is no simpler than designing your dream home. In some cases, you might even need some professional guidance.

Over the coming months, I will look at various ways in which you can make the most of your situation so you can confidently prepare the blueprints for building a retirement you can look forward to enjoying.

Issued by Total Risk Management Pty Ltd ABN 62 008 644 353, AFSL 238790 (TRM) as the trustee of the Russell Investments Master Trust ABN 89 384 753 567. This document provides general information only and has not been prepared having regard to your specific objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. The information has been compiled from sources considered to be reliable, but is not guaranteed. Any examples have been included for illustrative purposes only and should not be relied upon for the purpose of making an investment decision. Past performance is not a reliable indicator of future performance. The Product Disclosure Statement (PDS) can be obtained by phoning 1800 555 667 or by visiting russellinvestments.com.au. Any potential investor should consider the latest PDS in deciding whether to acquire, or to continue to hold, an investment in any Russell Investments product. The Target Market Determinations for the Russell Investments Master Trust are available on our website.

Russell Investment Financial Solutions Pty Ltd ABN 84 010 799 041, AFSL 229850 (RIFS) is the provider of MyTracker and the financial product advice provided via GoalTracker® Plus. TRM and RIFS are part of Russell Investments. Russell Investments or its associates, officers or employees may have interests in the financial products referred to in this document by acting in various roles including broker or adviser, and may receive fees, brokerage or commissions for acting in these capacities. In addition, Russell Investments or its associates, officers or employees may buy or sell the financial products as principal or agent. If you decide to purchase or vary a financial product, Russell Investments and/or other companies within the Russell Investments group of companies will receive fees and other benefits, which will be a dollar amount or percentage on the value of your investments and/or your insurance fees. You can ask us for more details.

General financial product advice is provided by RIFS or Link Advice Pty Ltd (Link Advice) ABN 36 105 811 836, AFSL 258145. Limited personal financial product advice is provided by Link Advice.

This work is copyright 2022. Apart from any use permitted under the Copyright Act 1968, no part may be reproduced by any process, nor may any other exclusive right be exercised, without the permission of Russell Investments.