Priorities today and save for tomorrow

Current costs are important but don’t take from the future to pay for the present.

By Hannah Tattersall - 3 min read

A little about Hannah

Hannah Tattersall writes about a range of topics, including personal finance, money and business.

My husband and I recently had the development application finally approved on our home renovation. We spent last year working with our architects on adapting our plans to accommodate council feedback, enlisting heritage consultants and arborists to provide information and documentation, and making sure we had the support of our neighbours—should we ever get to this place.

Well now we’re here, and yes, it’s exciting, but it also feels daunting. Because on top of our (increased) mortgage repayments, our usual family expenses and the rising cost of living, we now have to work out how to pay for it.

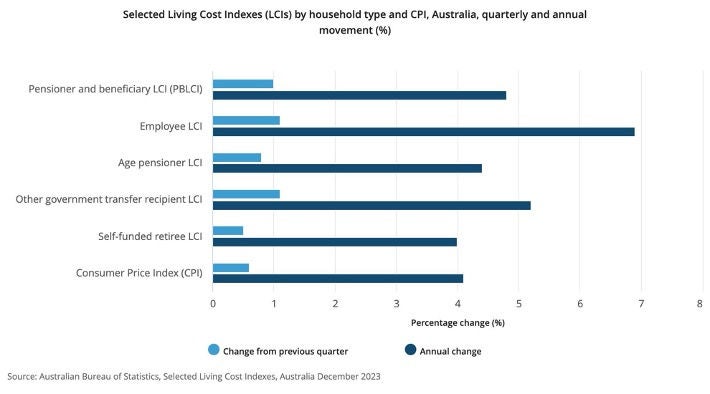

With so many competing demands (think mortgage or rent, school and daycare fees, food and bills, to name a few) many Australians are finding their finances are tighter than usual. In its most recent report on Living Cost Indexes (LCIs), the Australian Bureau of Statistics (ABS) revealed living costs for employee households rose 6.9 per cent in the year to 31 December 2023.

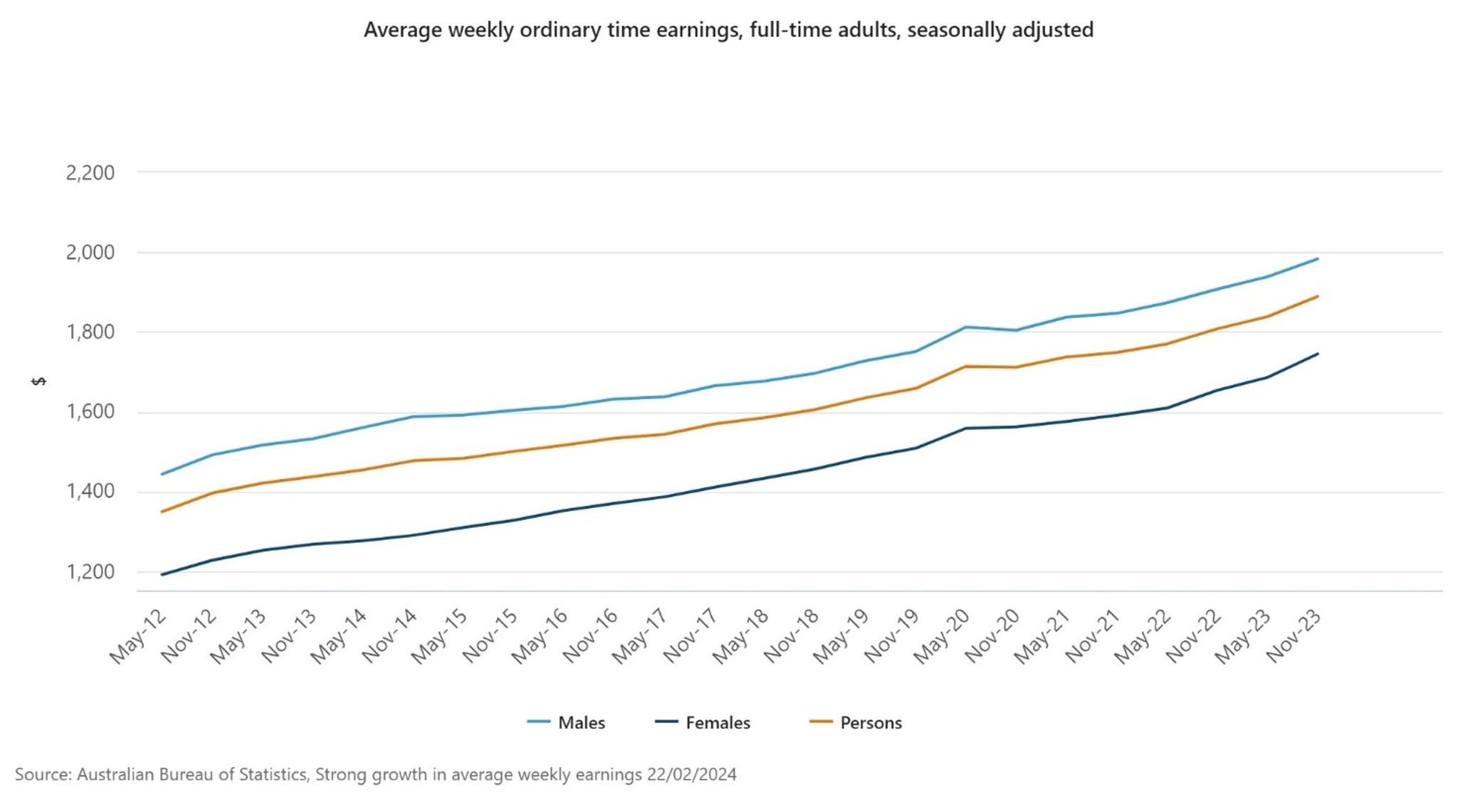

And while the cost of living is going up, average earnings have increased—specifically, the Average Weekly Ordinary Time Earnings increased by 4.5% for the year to 30 November 2023. While you might think this means more income—and it is—it also means a decrease in purchasing power when set against higher living expenses. And when the cost of living increases faster than our increasing incomes, our discretionary income (meaning what’s left over after taxes and essentials) is likely to decrease, which impacts our standard of living.

Setting priorities

For my husband and me, managing our money is about working out our priorities and budgeting to ensure we have enough to cover our expenses, both in the short term and the long term. We have been saving for our renovations for some time and have been factoring in an upcoming mortgage rate rise as well. Shopping around—whether it’s for a better home loan rate, cheaper groceries or a holiday deal—is now simply part of life.

Last year, we skipped going on holiday to save for our renovation, but it affected our mental health terribly. Some expenses (like for us, taking a holiday) are non-negotiable. Another is food. We have to eat. But these days we think twice about going out for a family meal or buying takeaway, as dining out has become so expensive.

Superannuation is another non-negotiable. Because I work as a contractor and freelance writer, at the end of each financial year I set aside a chunk of money to transfer into my super fund. I could decide not to do this this year in order to save more for our current living costs. But, due to the compound interest I'd be missing out on, I'd only be hurting my super balance in the long term.

We have a budget planner to keep track of ongoing immediate costs such as bills, food and groceries, meals out, childcare costs, extracurricular activities, gym memberships, haircuts and beauty expenses, gifts and clothes—and the list goes on. Once you list absolutely every cost in your budget planner, you realise where your biggest costs are and which areas to potentially cut back on.

Every little bit counts

There are other ways to save too, and while they may seem small, it all adds up over the course of a year.

Many people are opting to pay with cash again or use a debit card rather than a credit card to avoid unnecessary fees and surcharges, for example. Businesses incur costs for processing certain card payment types and some pass these on as a surcharge for paying with a card. As a guide, the Reserve Bank of Australia estimates the average cost for Eftpos is less than 0.5%; Visa and Mastercard debit is between 0.5% and 1%; and Visa and Mastercard credit is between 1% and 1.5%.

While a business must include the minimum surcharge payable in the displayed price for its products, it can still come as a surprise when you see the final amount you paid for an already inflated $5 coffee ($5.44 for me at one cafe recently) or an extra $1 on a purchase less than $10 if you’re paying by card.

I’ve become very fond of loyalty programs. As well as the big supermarket loyalty programs, many stores offer incentives for repeat purchasing. There are also ‘tenth coffee free’ cards at many local coffee shops (if you don’t want to cut your coffees altogether, these will at least save you some of the cost); and petrol programs offered by the major fuel retailers.

These small savings may not make a huge difference to our outgoing costs now, but they mean we’re not taking from tomorrow to pay for today. And we can look forward to a future where we have what we need—including a super balance to help fund our retirement—and hopefully even a renovated house.

Zest! recommends

SUPER 101

A Super way to buy your first home?

The First Home Super Saver Scheme could help you save more for your home deposit – here’s how.

By Jodie Cook

The views and opinions expressed in this article are those of the author and do not purport to reflect the views and opinions of Russell Investments.

Issued by Total Risk Management Pty Ltd ABN 62 008 644 353, AFSL 238790 (TRM) as trustee of Russell Investments Master Trust ABN 89 384 753 567. Nationwide Super and Resource Super are Divisions of the Russell Investments Master Trust. The Product Disclosure Statement (‘PDS’), the Target Market Determinations and the Financial Services Guide can be obtained by phoning 1800 555 667 or by visiting russellinvestments.com.au or for Nationwide Super by phoning 1800 025 241 or visiting nationwidesuper.com.au. Any potential investor should consider the latest PDS in deciding whether to acquire, or to continue to hold, an investment in any Russell Investments product. Russell Investments Financial Solutions Pty Ltd ABN 84 010 799 041, AFSL 229850 (RIFS) is the provider of MyTracker and the financial product advice provided by GoalTracker Plus. General financial product advice is provided by RIFS or Link Advice Pty Ltd (Link Advice) ABN 36 105 811 836, AFSL 258145. Limited personal financial product advice is provided by Link Advice with the exception of GoalTracker Plus advice, which is provided by RIFS.

This communication provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. If you'd like personal advice, we can refer you to the appropriate person. This information has been compiled from sources considered to be reliable but is not guaranteed. Past performance is not a reliable indicator of future performance. To the extent permitted by law, no liability is accepted for any loss or damage as a result of reliance on this information. This material does not constitute professional advice or opinion and is not intended to be used as the basis for making an investment decision. This work is copyright 2024. Apart from any use permitted under the Copyright Act 1968, no part may be reproduced by any process, nor may any other exclusive right be exercised, without the permission of Russell Investments.