Keep calm and carry on: key takeouts from February’s reporting season

Investors would do well to pause and take stock after the recent reporting season rather than over-react to the relatively benign results from Australian companies.

The biggest takeaway from the results was that the full impact of inflation and rising rates on the consumer is not yet evident and may not be apparent for another 6-12 months.

Outlook statements issued by management highlighted the extent to which inflation and stubbornly higher costs for companies are creating downside risks for margins in a slowing economy.

In this context, the slightly disappointing results were not unexpected and instead a signal to the market to remain in “wait and see” mode until the risks that have dominated markets for more than a year play out.

The divergence in company reporting, and underperformance in companies which had benefited in the post-COVID environment, were headwinds for Russell Investment’s High Dividend Australian Share ETF (RDV) over the month of February.

Final tally

At an aggregate level, forecast earnings growth for full year 2023 were downgraded after reporting season to around 5%, from 7%1 previously, and are expected to decline again next financial year. Most of the downgrades are at the smaller end of the market.

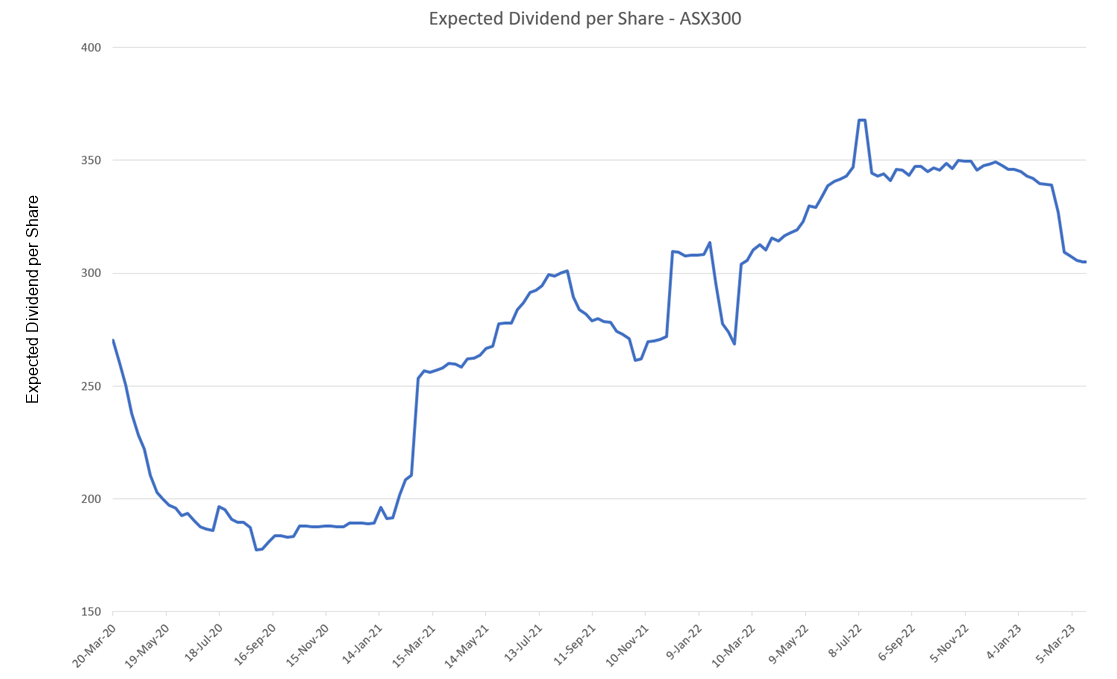

Dividends were similarly trimmed but, as a whole, the market continues to provide the relatively consistent yield that is often an attraction for investors in Australian shares.

However, idiosyncratic volatility around results impacted RDV’s performance in February. Aurizon Holdings and JB Hi-Fi have been held due to strong dividend characteristics but both reported a soft result which negatively impacted their share prices.

Click image to enlarge

Source: Bloomberg

Dividends from the materials sector were a bright spot, with BHP’s expected yield just under 7% despite a disappointing result driven by softening commodity prices and 40% cut to its interim dividend.2 Rio Tinto was also among the top dividend payers.

Insurers stand out

The insurance sector provided another highlight with companies such as Suncorp, QBE and Medibank all beating profit expectations as a result of higher written premium and the tailwind provided to insurers by higher interest rates. Suncorp and Medibank are held at an overweight position in RDV, and added value over the month of February. Both stocks maintain a positive outlook for dividends, which should benefit RDV shareholders.

Elsewhere in financial services, major banks delivered earnings in line with market expectations but the commentary that accompanied Commonwealth Bank of Australia’s results suggested the bulk of the uptick in net interest generated by rising rates may be behind us.

A bigger focus on climate change and ESG more broadly was evident in company reports as management sought to improve the disclosures that allows shareholders to better understand the sustainability risks that apply to individual stocks. This trend will continue, including in sectors which have less obvious exposure to climate change, as both institutional and retail shareholders demand a more robust view of company operations.

Key takeaways

Russell Investments believes the best tack in the current environment is to stay focused on quality – or companies that demonstrate pricing power, reasonable gearing and strong profitability. There is also a case to pull back on cyclical stocks that are more directly linked to the overall state of the economy and will come under pressure if the latter slows.

Volatility will remain heightened as the market adjusts from the low interest rates and low inflation environment that prevailed during the height of COVID to those that are dominant today. The big question now is how quickly, and high, interest rates will rise, a question complicated by the collapse of Silicon Valley Bank.

1, 2 Bloomberg