The RBA surprise with a hike

The Reserve Bank of Australia (RBA) surprised the market, raising rates by 0.25% to 3.85%. This is the eleventh rate hike since they embarked on raising rates last year. Despite raising rates, the language used in the RBA statement was more measured when discussing the outlook – indicating that we are now likely at the end of the hiking cycle.

To understand why the market was surprised by this rate decision, it is valuable to rewind back to last month when the RBA left rates on hold. The RBA noted that the monetary policy operates with long and variable lags. For this reason, they wanted to give themselves a chance to see how the rate hikes were impacting the economy. More importantly, they wanted to see the impact it had on consumer spending, the labour market and obviously inflation.

Following the meeting, RBA Governor Lowe gave a speech where he focused on some of the inflationary impacts of three specific supply side challenges:

- the Australian rental housing market

- the electricity market, and

- depressed labour productivity.

The focus on supply side indicated that the RBA were quite comfortable with the amount of work they had undertaken on the demand side of the economy.

What drove the increase in the cash rate?

Now, fast forward to today. The increase in the cash rate was driven by three things.

- The forecasted path to lower inflation was still deemed too slow by the RBA.

- Overseas experience indicates that some services inflation could be more sticker i.e. less easily slowed.

- The labour market remains tight with the unemployment rate still around 50-year lows.

The next question to ask is whether this changes the outlook for the Australian economy. Our view is that bar further potential rates hike(s) from the RBA this year, these changes don't represent a big shift in the economic outlook. The economy should still eke out reasonable growth this year, aided by the return of immigration. The RBA themselves have reduced their GDP forecast this year to 1.25%, which is not a stellar result, but in a year of slowing global growth and recession risk, it is not too bad.

Key watchpoints for the economy in the coming months

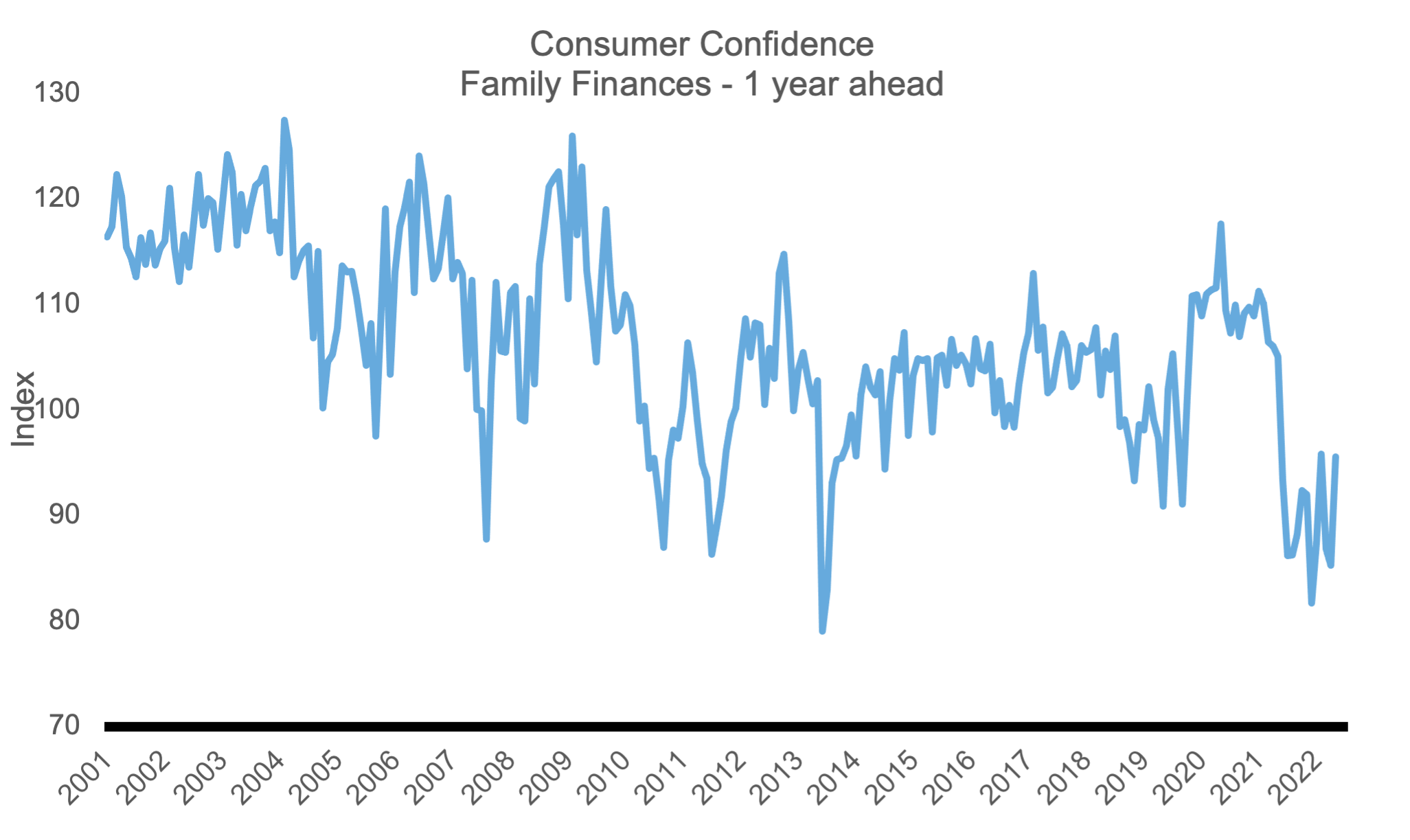

1. Consumer spending and confidence. The wave of fixed rate mortgage resets has begun, and we will see a reduction in disposable income for those households impacted. Whilst we have seen consumer confidence rebound in the last couple of months, we suspect this could be vulnerable to a reversal given the unexpected increase in interest rates.

Source: Refinitiv Datastream, 2 May 2023

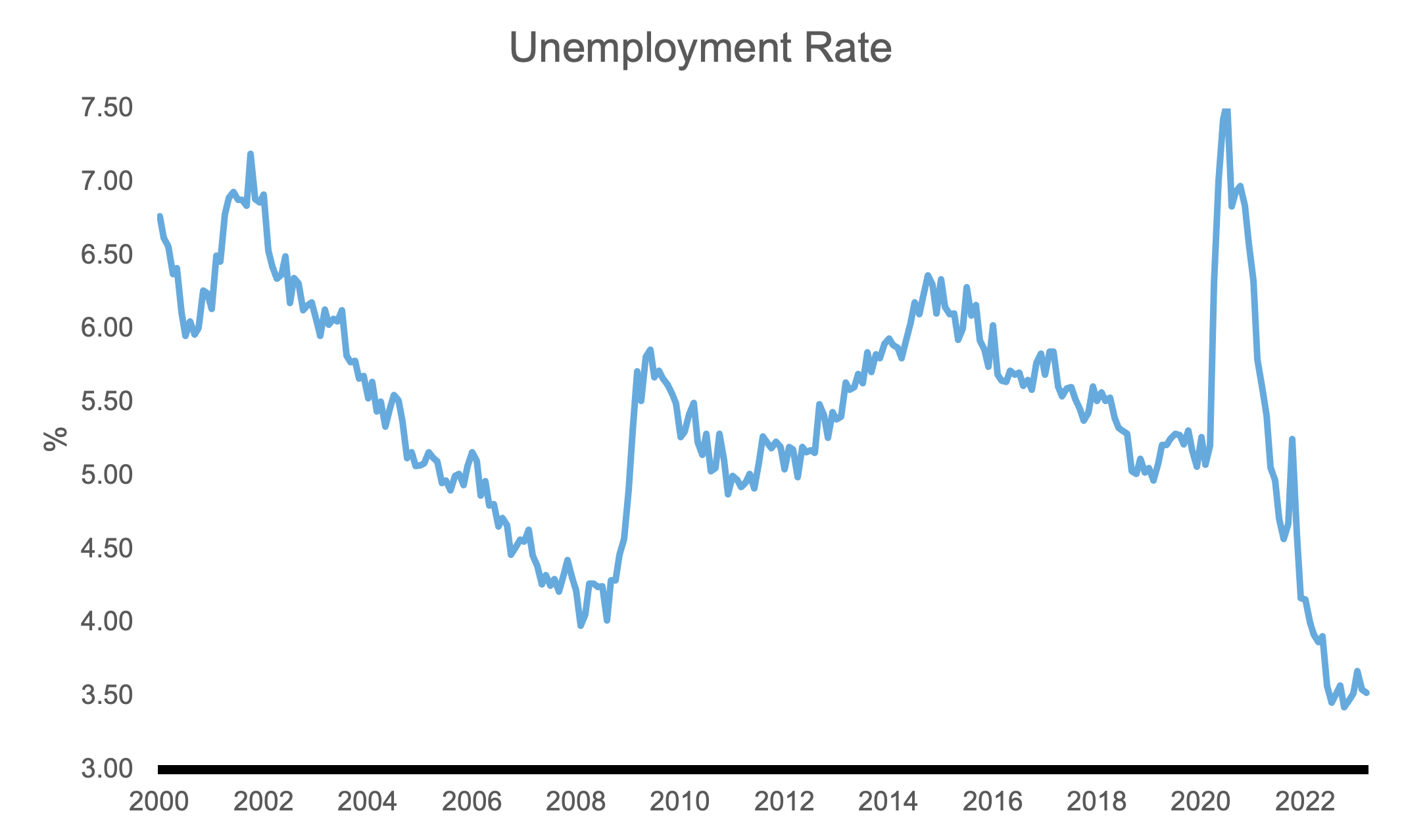

2. The strength of the labour market. As mentioned above, one of the issues that the RBA has flagged is the low level of labour productivity. This is concerning because it lowers the rate of wage growth that is consistent with the inflation target. This means that any increase in wages without a commensurate improvement in labour productivity could lead to future interest rate increases from the RBA Hiring intentions and job vacancies are also important factors, which indicate how well the increase in the labour force (due to immigration) will be absorbed in the economy.

Source: Refinitiv Datastream, 2 May 2023

Looking ahead, the RBA did soften the language around further rate rises, but are still noting that further rate increases may be needed. Governor Lowe gave a speech overnight in Perth and commented that it would be a good outcome if inflation came back to the top of the target range by mid-2025 – hinting that this is the timeline through which to judge future rate hikes. We believe that Australia has likely reached the end of the hiking cycle. However, it is possible that there is one more rate hike, if the data surprises to the upside in the coming months.