Super strong in volatile times

There’s been increased talk of market volatility, high inflation and investment returns over the past few weeks. How has it impacted your super – after all it’s one of the biggest investments you are likely to make. We spoke to our in-house investment strategist to find out more.

By Alex Cousley - 4 min read

A little about Alex

Alexander Cousley is the Asia-Pac Investment Strategist for Russell Investments. He is responsible for covering the Asian region, as well as listed real assets.

Market volatility is usually part and parcel of investing and most of us are guided by that well-worn saying that time in the market is better than timing the market.

However, when the daily news cycle is saturated with messages about volatility, rising inflation, high interest rates, global recession, geopolitical conflicts, etc. it can be challenging to keep calm and carry on. Add to that, we’re all trying to adjust to a post-pandemic way of living.

That’s why we sat down with our in-house investment strategist to ask him a few questions about what exactly is going on and how best to weather this latest storm.

1. There’s so much uncertainty in the markets – what’s going on?

There is a huge amount of things going on—but the most important development right now is the far more aggressive approach to raising rates that central banks are taking in the face of stubbornly high inflation.

At the start of the year, the market was expecting 3 increases of 0.25% each from the United States Federal Reserve for 2022. As we stand now, the market expects that the Federal Reserve will have raised rates by the equivalent of 13 increases for 2022.1

On top of that, we have also had the ongoing conflict in Ukraine and the pressure that has placed on commodity prices and the COVID lockdowns in China.

2. We’ve not seen this kind of persistently high inflation for a long time. What is the impact of inflation on markets?

High inflation has a negative impact on asset markets, especially equities and government bonds. On the equities front, it can put pressure on companies’ profit margins (not all companies are able to or want to pass on higher borrowing costs to their customers in the same way) as well as the multiple that investors are willing to pay for a dollar of earnings.

Inflation also deteriorates the purchasing power of currency, which means that government bonds—which provide fixed payments through the future—become less valuable.

3. How does all this impact my super and what is Russell Investments doing to manage the situation?

Investment returns since the start of the year have been weak, given the sell-off in both equities and government bonds. Global equities are down close to 20% (using the MSCI All Country World Index), while government bonds have fallen by 9% (using the Bloomberg Global Treasury Index). For a point of comparison, this has been one of the worst first halves for both equities and bonds in recent history.

At Russell Investments, we had reduced some of the risk in our portfolios in the lead up to this by selling some of our equity and credit positions. We continue to monitor the portfolios and markets very closely, and are maintaining a very disciplined approach to investment decisions.

4. Why is it that defensive options are not particularly defensive this year?

High inflation is one of the main reasons—it has come in much higher than many had expected. Most defensive assets provide some level of fixed income, and inflation erodes the value of those future fixed payments. Additionally, the raising of interest rates by central banks has also reduced the value of those defensive assets, as cash rates have risen and provided some investors with a more attractive risk-free return.

However, as we look ahead, we do think that a lot of the bad news is now priced into these defensive assets—and in some cases, is starting to present attractive valuations.

5. Super is a long-term investment, but how can I keep my calm when markets are in so much turmoil?

It’s extremely important to stick to your investment plan, especially in very volatile times. Often, reacting to volatility can lead to poor decision making. For example, during the COVID experience Australia saw a lot of investors sell equities to cash, and then never manage to get back into the equity market, which saw a very large rally.

At Russell Investments, our disciplined approach of assessing the cycle, valuation and sentiment minimises the behavioural biases that humans are susceptible to—and we make sure that all the funds in the Russell Investments Master Trust investment menu maintain this discipline through the market cycle.

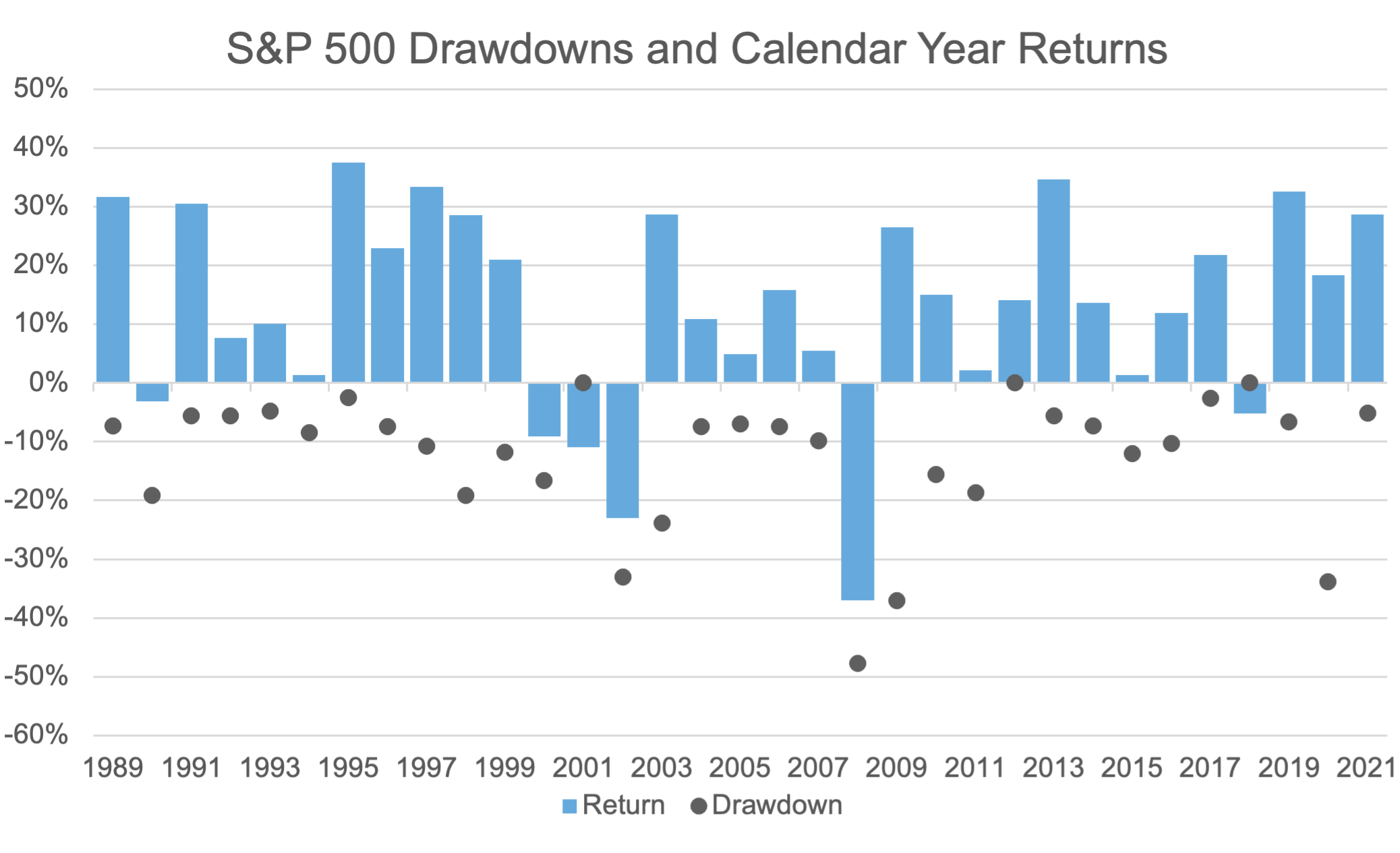

Finally, it’s always important to zoom out and look at the longer-term—markets have gone through these episodes of volatility plenty of times in the past. The chart below shows the drawdown in equity markets in any given year, and the final return for the year—as you can see, drawdowns of 15-20% are actually quite common in any given year. Importantly though, many of those years ended up with positive returns.

When it comes to deciding what you should do during times like this, the first step is to not panic, and for most people the next step is to do nothing. Every crisis and every market downturn come to an end—there has never been an exception to this rule.

Source: Refinitiv Datastream, 30 June 2022.

6. What can Russell Investments do to help me stay the course?

While we can’t predict with any certainty how markets evolve, we do provide a number of resources on our website and blog, including commentary on what is happening in the markets and how we are responding to them. We also offer webinars and forums, where you can hear the latest on how Russell Investments is positioned and see opportunities.

Finally, remind yourself that your investment strategy is suited to your personal circumstances—it is designed to weather these storms and recover in due time. If you haven’t looked at your investment strategy in a while, we encourage you to do so today.

If you need more help to personalise the way you invest your super, check out our GoalTracker® program. It’s designed to take the guesswork out of super and help you to set a goal for how much income you’ll need to fund your desired lifestyle in retirement. Additionally, GoalTracker Plus takes your circumstances and retirement income goal into consideration and creates a personalised investment strategy.

1 Refinitiv Eikon, 4 July 2022.

Issued by Total Risk Management Pty Ltd ABN 62 008 644 353, AFSL 238790 (TRM) as trustee of Russell Investments Master Trust ABN 89 384 753 567. Nationwide Super and Resource Super are Divisions of the Russell Investments Master Trust. The Product Disclosure Statement (‘PDS’), the Target Market Determinations and the Financial Services Guide can be obtained by phoning 1800 555 667 or by visiting russellinvestments.com.au or for Nationwide Super by phoning 1800 025 241 or visiting nationwidesuper.com.au. Any potential investor should consider the latest PDS in deciding whether to acquire, or to continue to hold, an investment in any Russell Investments product. Russell Investments Financial Solutions Pty Ltd ABN 84 010 799 041, AFSL 229850 (RIFS) is the provider of MyTracker and the financial product advice provided by GoalTracker Plus. General financial product advice is provided by RIFS or Link Advice Pty Ltd (Link Advice) ABN 36 105 811 836, AFSL 258145. Limited personal financial product advice is provided by Link Advice with the exception of GoalTracker Plus advice, which is provided by RIFS.

This communication provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. If you'd like personal advice, we can refer you to the appropriate person. This information has been compiled from sources considered to be reliable but is not guaranteed. Past performance is not a reliable indicator of future performance. To the extent permitted by law, no liability is accepted for any loss or damage as a result of reliance on this information. This material does not constitute professional advice or opinion and is not intended to be used as the basis for making an investment decision. This work is copyright 2022. Apart from any use permitted under the Copyright Act 1968, no part may be reproduced by any process, nor may any other exclusive right be exercised, without the permission of Russell Investments.