Dividend based ETFs – Stock and Sector Positioning to Emerge from the Pandemic

Dividends have been an important driver of the returns from Australian shares for many years.

The Australian share market has been one of the highest yielding markets globally producing 4%+ p.a. of income over the last decade for investors with the added benefit of franking credits. When Russell Investments High Dividend Australian Shares ETF (ticker RDV) hit its 10-year anniversary earlier this year, it had delivered investors that invested at launch an average 6% p.a. of income.1

Covid-19 has not only seen interest rates approach zero, it has had a dramatic effect on the outlook for dividends. APRA’s capital management recommendations in April 2020 resulted in many financial institutions cancelling dividends. However, ahead of reporting season APRA relaxed guidelines which allowed several banks and insurers to pay dividends in August, albeit at lower levels than we have become accustomed to. Expected dividends for the S&P/ASX 200 had dipped to around 3% for the next 12 months as a result.

This note highlights key moves from our recent index rebalance in RDV and RARI (Russell Investments Australian Responsible Investment ETF). Both ETFs have an income objective and have yielded well above the S&P/ASX 200 historically. Therefore, the stock and sector changes in the ETFs, using recent data and forward-looking expectations for dividends, provide some useful insight on how to maintain a healthy level of income from a portfolio of Australian shares.

REITs

Many yield-based strategies in Australian shares shun Real Estate Investment Trusts (REITs) as they do not pay franking credits. Our ETF methodology however evaluates all securities on a ‘grossed-up basis’ i.e. including franking credits. REITs can still be an attractive income-based investment as distribution income can be comparable to, or higher than, other stocks including franking credits. The common theme from the recent ETF rebalances was a net purchase of REITs. Separately, we have also been adding to REITs across other active Russell Investments funds given their relative attractiveness from a valuation perspective and our outlook for the economy:

Source: Russell Investments.

REITs have historically traded at a slight premium to the market but are currently trading at a significant discount. Much of this reflects the concern around demand for real estate after the pandemic – particularly for retail-based REITs such as Australian Westfield operator Scentre Group. However, we believe that the current valuation discount has already priced in these concerns. It is worth noting that most REITs still paid dividends in June and we expect the same when most REITs pay their first dividend of the Financial Year in December. Both RDV and RARI are now overweight REITs.

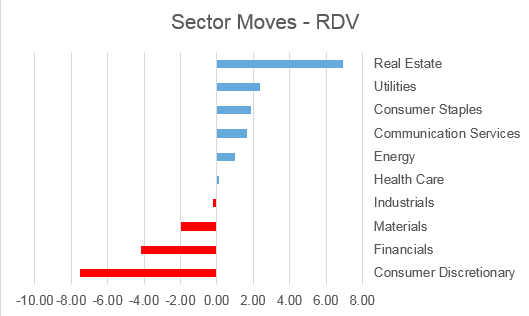

RDV Rebalance – September 2020

The table below shows the sector changes what we implemented:

Source: Bloomberg.

The buy of REITs is a clear stand-out which was funded by a net sell of consumer discretionary stocks. Consumer discretionary stocks have been one of the top performing sectors of the last six months (we previously rebalanced the ETFs in March 2020). Whilst consumer stocks have done well, their yield credentials have diminished following a 40% bounce in their share prices. Harvey Norman has been a winner for RDV over the last six months, but the position was exited in October after collecting the most recent dividend. Harvey Norman’s dividend policy has been a wild ride in 2020 – the April dividend was cancelled just before pay-date, and the company then made an out-of-cycle dividend payment just before financial year end. It appears to be an opportune time to take profits for now after this month’s 4% dividend and strong share price performance.

RARI Rebalance – September 2020

The table below shows key sector moves for RARI:

Source: Bloomberg.

REITs were a net buy for RARI due to both positive ESG scores and yield credentials. RARI is diversified across 14 different REITs and has a significant overweight at the sector level versus the S&P/ASX 200. This overweight was funded by a sell of financials due to lower dividend expectations, and a sell in materials stocks. Materials stocks, a 20% weight in the S&P/ASX 200, have outperformed in the last six months and have been a more reliable source of dividends than many other sectors. RARI does not hold index heavyweights BHP or Rio Tinto due to fossil fuel-based exclusions, however does hold other Materials stocks such as Fortescue Metals that score better on ESG characteristics. In addition, Fortescue Metals has delivered healthy dividends during the pandemic fuelled by a strong iron ore price. RARI was a net seller of Fortescue in the recent rebalance but remains overweight.

Not Out of the Woods Yet

Covid-19 continues to challenge the business models of companies across most sectors of the market. Investors seeking income from an Australian shares portfolio are encouraged to diversify in such an environment. Both RDV and RARI offer such a solution with a robust methodology that screens for yield using five underlying factors. Analyst forecasted 12-month dividend yield is given the highest weight in our methodology, such that the methodology tilts to expected futured dividends rather than buying ‘last year’s income’. We also seek stability of earnings when determining the relative attractiveness of a stock’s income characteristics. Both ETFs have started Q4 strongly following their reconstitution and look well placed to continue to deliver yields in excess of the broader market.

1 Bloomberg - based on actual distributed income net of fees and charges.

IMPORTANT INFORMATION

Issued by Russell Investment Management Ltd ABN 53 068 338 974, AFS License 247185 (RIM). This communication provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. Any potential investor should consider the latest Product Disclosure Statement (PDS) for the Russell Investments High Dividend Australian Shares ETF (RDV) in deciding whether to acquire, or to continue to hold, units in the ETF. Only persons who have been who have been authorised as trading participants under the Australian Securities Exchange (ASX) Operating Rules can apply for units in the ETF through the latest PDS. Investors who are not Authorised Participants looking to acquire units in the ETF cannot invest through the PDS but may purchase units on the ASX. Please consult your stockbroker or financial adviser.

The Russell Australia High Dividend Index (the “FRC Index”) is a trademark of Frank Russell Company (“FRC”) and has been licensed for use by Russell Investment Management Ltd. RDV is not in any way sponsored, endorsed, sold or promoted by FRC, FTSE Russell or the London Stock Exchange Group companies (“LSEG”) (together the “Licensor Parties”) and none of the Licensor Parties make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to (i) the results to be obtained from the use of the FRC Index (upon which RDV is based), (ii) the figure at which the FRC Indexes is said to stand at any particular time on any particular day or otherwise, or (iii) the suitability of the FRC Indexes for the purpose to which it is being put in connection with RDV. None of the Licensor Parties have provided or will provide any financial or investment advice or recommendation in relation to the FRC Index to Russell Investment Management Ltd or to its clients. The FRC Index is calculated by FRC or its agent. None of the Licensor Parties shall be (a) liable (whether in negligence or otherwise) to any person for any error in the FRC Index or (b) under any obligation to advise any person of any error therein.

For any ESG considerations, please refer to the Product Disclosure Statement for the Fund - Russell Investments Australian Responsible Investment ETF

Copyright © Russell Investments 2020. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.