Your superannuation can be used in conjunction with the Age Pension (from age 67, if you are eligible for the Age Pension).

That means you can access your super savings to top up or supplement any Age Pension amount you may receive. The GoalTracker tools account for the Age Pension when calculating your projected income in retirement and how long your super may last.

4. Explore your options

As retirement gets closer and you’re about to reach the age when you can turn your super into an income, it’s time to consider how and when is right for you.

That means understanding your options and working out whether you want to keep working part-time or retire altogether.

Being prepared is always a good idea – as there’s also the possibility that the timing of your retirement could happen suddenly due to a health event or change in employment.

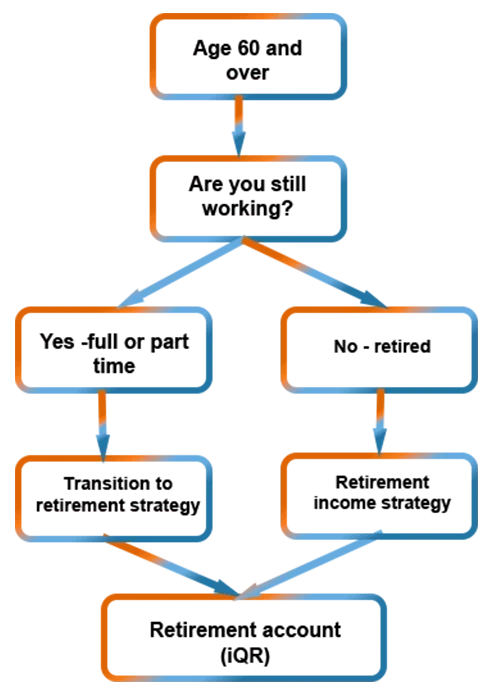

Here’s a snapshot of the options available once you reach your preservation age of 60, depending on your work situation.

Get help to understand your options

This interactive tool will help guide you through your options as you get closer to the age where you can choose to access your super.

You’ll be asked some simple details about yourself and your current circumstances. Based on your responses, you’ll get insights and details of actions you can explore further. Like some help to work out whether you want to keep working – either full or part-time, or retire altogether, and then how you can generate an ongoing income depending on your work situation.

It's like a ‘choose your own adventure’ based on your super savings and how you can make the move towards retirement.

When can you access your super?

Generally, you can only access your super when you reach your ‘preservation age’. If you were born after 1 July 1964, that will be age 60. If you were born any earlier, you will have already reached it. To access your super, you’ll also need to either retire from work altogether or start a Transition to Retirement (TTR) income stream while you keep working.

Once you reach age 65, you can access your super and turn it into an income, even if you’re still working full-time.

This Fact Sheet includes details about when you can access your super. There are some limited situations where you can access your super early – that’s also detailed by the ATO here.

A modern take on retirement

It used to be common that when you retired, you accessed your super as a lump sum payment and off you went.

Today though, we’re living and staying healthy longer, and most of us are now choosing to work longer, too – even if that means dropping back to a few days a week.

Once you’ve reached your preservation age, you can stop working and open a retirement account (also called an Account Based Pension), like our iQ Retirement account, to access your super as a regular payment.

You can also choose to ease into your retirement with a Transition to Retirement (TTR) strategy. You can open an iQ Retirement account that lets you use your super to provide an income stream. Then, you can either work part-time and top up your take-home pay with a regular income from your super, or continue working full-time and use iQ Retirement to boost your income or super (via salary sacrifice).

However you choose to use iQ Retirement, your super savings stay invested - even while you’re drawing an income, which means that your super can continue to earn returns. There’s also plenty of flexibility and you keep control over the payment amount and frequency.

Need help?

There may be lots of information to take in and options to consider at this stage of your journey, but you shouldn’t feel overwhelmed - we’re here to help.

Good support can help set you up for success – but it’s worth noting that not all guidance and advice is the same. You have access to a wide range of support and advice options, often at no cost, and we’re here to help work out which one is right for you.

Simply request a callback for a time that suits you and we’ll talk you through your options.

Retire Ready appointments*

A one-on-one meeting with a Retirement Consultant to give you general information on your retirement options and things to consider regarding your super as you approach retirement

Simple phone advice

Targeted, personalised advice on how to maximise your super – over the phone with an expert

Help on topics specific to your super like investment strategy, contributions, insurance, pension and transition to retirement

RetireAssist

For members within 12 months of retirement

Covers a broad range of topics like estate planning, debt management, Age Pension and strategic advice for your partner, plus more

A cost-effective alternative to comprehensive advice delivered over the phone

Comprehensive advice

Personal financial planning advice that takes your full financial picture, including assets outside super, into account

Tailored advice from a financial adviser we have partnered with on our panel

*A Retire Ready meeting includes General Advice and doesn’t take into account your goals, personal/financial circumstances or retirement needs.

Is a TTR right for you?

There are generally three ways to use TTR as you approach retirement.

Lifestyle booster

Reduce your working hours (for example, by moving to part-time work) and maintain your current take-home pay.

Super booster

Increase your super savings without affecting your day-to-day income by contributing more of your earned income to super (via salary sacrificing).

Income booster

Top up your current income while continuing to work the same number of hours, while also saving on tax to boost your retirement income.

The aim is to strike the right balance between making super contributions, drawing TTR income payments, and generating your required cash flow.

Case Study - HOW STEVE BOOSTS HIS BALANCE

Simply by using a TTR strategy, Steve is able to boost his retirement savings by an extra $3,946.

Steve, 60, is still working full time, earning $70,000 plus his super guarantee contribution, and plans to retire when he is 65. With five years up his sleeve, he wants to bolster his retirement savings. While he will be limited by his concessional contributions cap of $30,000 a year, he sets up an iQ Retirement account so he can start a TTR strategy and salary sacrifice more into his super.

Steve salary sacrifices as much of his salary as possible into his existing super account, and draws down an amount from his pension account, so that he still has the same amount of money on which to live. The maximum he may draw down is 10% of his pension account.

In one year, Steve could improve his financial position by paying less tax and having this amount invested in his iQ Retirement account. If Steve continued with this strategy for 5 years, Steve would boost his super by close to $20,000 (plus any additional investment earnings), while keeping the same take-home pay.

The illustration above is based on the tax rates and limits applying for the 2025-26 financial year (Income Tax includes the Medicare Levy); and is net of the Low Income Tax Offset. The superannuation guarantee is 12% and, for the 2025-26 financial year an individual can make a before tax contribution to super of up to $30,000. Example shown for illustrative purposes only.

Government Age Pension

A different type of pension that is funded by the Government (not your super savings) is the Age Pension.

Most Australians can apply for the Age Pension from age 67. The amount you’ll be entitled to (if any) depends on an income and assets test, which includes your super. It’s worth noting that you may become eligible for the Age Pension at some point in the future, even if you don’t qualify to start with.

If you’re entitled to the Age Pension, it will be an income source for life. Though it’s becoming increasingly difficult to fund a comfortable retirement on the Age Pension alone – which is where your super savings come in handy.

You’ll also be eligible for other discounts and allowances like a Pensioner Concession Card or a Commonwealth Seniors Health Card, which can help with the cost of health care and medicines. Add to that the discounts on utility bills, property and water rates, transport fares and motor vehicle registrations, the benefits can bring valuable savings to your budget.

FAQs

The short answer is no, you’re not locked in. You can always go back to full-time or part-time work, and consider making changes to salary sacrifice arrangements etc. Your super can ‘roll-back’ to the ‘accumulation’ or ‘contribution’ phase.

It’s always a good idea to understand your options and plan ahead, even if you’re still a couple of years from reaching your preservation age.

Reaching preservation age doesn’t necessarily mean you stop working, but it does mean you can consider making your super savings work for you, as you’re able to access them to start providing you a regular income. There are also options that let you ease into retirement, such as a transition to retirement (TTR) pension, which allows you to work part-time while you begin drawing on your super. There’s plenty of information on this page about TTR and whether that strategy may be right for you.

As you near your preservation age and retirement, your investment strategy should reflect your circumstances at that point in time, including the level of risk you’re comfortable taking with your investments.

You should also be checking regularly whether or not you’re already on track to your retirement income goal, and the GoalTracker ‘tracker dial’ in your online account is a good place to start. There’s tools available there that help you simulate the potential impact of things like changing your retirement age or making different levels of additional contributions into super.

If you completed Step 2 of the Pathway and used the GoalTracker tools to get an income projection and set a retirement income goal, you’ll be able to login to your account and see the ‘tracker dial’ which will show whether you’re on track. With GoalTracker you can also simulate the potential impact of things like changing your retirement age or making different levels of additional contributions into super.

You could also consider a Transition to retirement (TTR) strategy which can be utilised to grow your super through tax savings - without decreasing your take home pay.

Plus, we’re always here to help if you need some personal advice to understand your situation with the help of a qualified adviser. Just get in touch.