Drawing retirement income from your home

Your home is more than just a place to live—it can also be a source of income in retirement.

By Joel Atputharaj - 3 min read

A little about Joel

Joel Atputharaj is a senior manager at Russell Investments. A Fellow of the Institute of Actuaries and a registered Financial Adviser, he helps clients navigate complexity and has worn many hats across the superannuation and consulting businesses, Joel is currently leading a program of work to enhance the Russell Investments offer to those who are approaching, at or in retirement.

There’s an old saying ‘you can’t have your cake and eat it too’—but the same doesn’t apply to houses. With home equity release, you can keep your home and use its equity for retirement income.

Even receiving relatively small portions of home equity as retirement income can substantially improve your lifestyle in retirement.

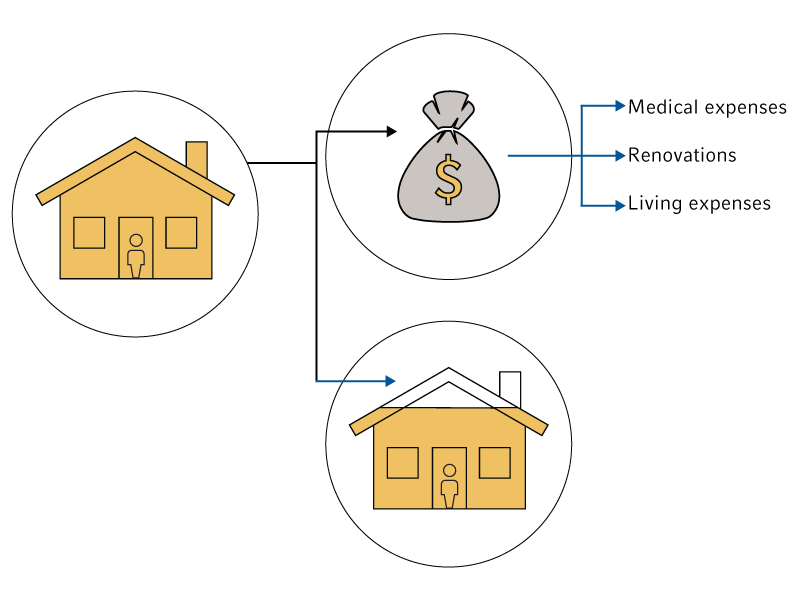

What is home equity release?

Equity is the value of your home that you own, excluding your mortgage or other debt you may have secured against that property.

Equity release allows you to take some of your equity out of your home and use it for other purposes, such as to pay for medical expenses, renovations or general living costs.

The amount of money you can draw from your home depends on:

- your age

- the value of your home

- how much equity you own in the property

- the type of equity release.

Equity release options

There are several types of equity release.

The Australian Government offers the Home Equity Access Scheme (formerly known as the Pension Loans Scheme).

Some private companies offer:

- reverse mortgages

- home sale proceeds sharing / home reversion products

- equity release agreements

What are the Pros and Cons?

Generally, the common features of these products are that you:

- are over 60 to access them

- Need to own your home outright or own your home with a mortgage

- Can take money out of your home while you continue to live in the property.

Each arrangement has different conditions and costs associated – and there can be implications for your family members and other people you live with. It’s essential to understand the details before you sign up.

You can read more about each type of home equity release product at Moneysmart.gov.au.

For more on the Home Equity Access Scheme, you can contact the Centrelink older Australians line or the Services Australia Financial Information Service. Independent financial advisers and legal professionals can also assist.

How can it fit into a retirement income strategy?

Withdrawing money from your home may allow you to supplement your regular income so you can live a more comfortable lifestyle in retirement. It could also help you pay for a one-off expense, so you don’t have to save up your regular income (from your superannuation or government age pension, for example) to cover the cost – or sell and move out of your home.

Home equity release options won’t be right for everyone but knowing that you can tap into your home’s equity can provide the comfort of an extra source of funds, should you need it.

Questions to consider

- How much can you get?

- How will the arrangement affect your ownership of your property?

- How much will the repayments, interest and/or fees cost in total?

- When, and how, will you need to make repayments, or will it just be on the sale of your property (e.g. when deceased)?

- Can the equity you release be taken as an income stream or a lump sum, or a combination of the two?

- How will it affect your eligibility for the Government Age Pension? How does it impact your Age Pension entitlement i.e. how much will you receive?

- Will someone else who lives in your home with you be able to stay in the property when you move out or die?

- Do you fully understand the fine print of the agreement (if not, seek legal or professional advice)?

Zest! recommends

* The opinions expressed are those of Dr Jon Glass and 64Plus. Russell Investments does not endorse, and is not accountable for, any views expressed by Dr Jon Glass or 64Plus.

Issued by Total Risk Management Pty Ltd ABN 62 008 644 353, AFSL 238790 (TRM) as trustee of Russell Investments Master Trust ABN 89 384 753 567. Nationwide Super and Resource Super are Divisions of the Russell Investments Master Trust. The Product Disclosure Statement (‘PDS’), the Target Market Determinations and the Financial Services Guide can be obtained by phoning 1800 555 667 or by visiting russellinvestments.com.au or for Nationwide Super by phoning 1800 025 241 or visiting nationwidesuper.com.au. Any potential investor should consider the latest PDS in deciding whether to acquire, or to continue to hold, an investment in any Russell Investments product. Russell Investments Financial Solutions Pty Ltd ABN 84 010 799 041, AFSL 229850 (RIFS) is the provider of MyTracker and the financial product advice provided by GoalTracker Plus. General financial product advice is provided by RIFS or Link Advice Pty Ltd (Link Advice) ABN 36 105 811 836, AFSL 258145. Limited personal financial product advice is provided by Link Advice with the exception of GoalTracker Plus advice, which is provided by RIFS.

This communication provides general information only and has not been prepared having regard to your objectives, financial situation or needs. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. If you'd like personal advice, we can refer you to the appropriate person. This information has been compiled from sources considered to be reliable but is not guaranteed. Past performance is not a reliable indicator of future performance. To the extent permitted by law, no liability is accepted for any loss or damage as a result of reliance on this information. This material does not constitute professional advice or opinion and is not intended to be used as the basis for making an investment decision. This work is copyright 2022. Apart from any use permitted under the Copyright Act 1968, no part may be reproduced by any process, nor may any other exclusive right be exercised, without the permission of Russell Investments.